Australia Green Hydrogen Market Overview:

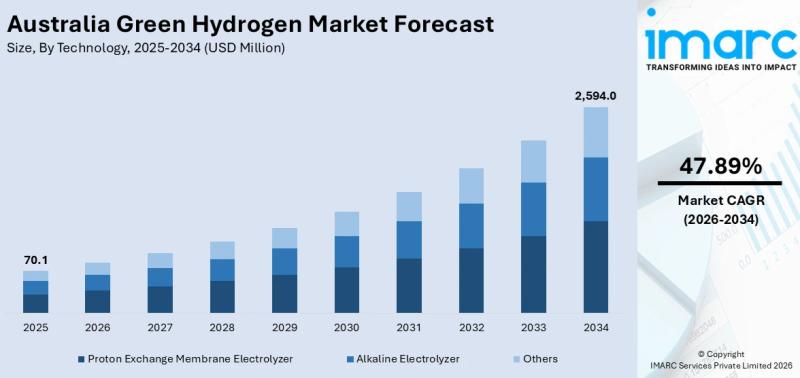

Australia is betting big on green hydrogen, with massive government production tax credits, billion-dollar export projects, and international partnerships positioning the country to become a global clean fuel powerhouse by the end of the decade. The Australia green hydrogen market size reached USD 70.1 Million in 2025. Looking forward, the market is expected to reach USD 2,594.0 Million by 2034, exhibiting a growth rate (CAGR) of 47.89% during 2026-2034. The market encompasses diverse technologies, applications, and distribution channels tailored to Australia’s evolving clean energy landscape, covering proton exchange membrane electrolyzers, alkaline electrolyzers, and other technologies across power generation, transport, and other applications, distributed via pipeline and cargo channels spanning Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & South Australia, and Western Australia. Coordinated government incentives, including the Hydrogen Production Tax Incentive and concessional financing, strategic international collaborations with partners in Japan, South Korea, and the EU, expanding port-based hydrogen hubs, and standardized certification schemes are some of the key factors driving market growth throughout the forecast period.

Read more about Australia Green Hydrogen Market:

https://www.imarcgroup.com/australia-green-hydrogen-market/

Australia Green Hydrogen Market Summary

• Massive ARENA Funding for Murchison Project: On March 20, 2025, ARENA announced $814 Million in conditional funding for Copenhagen Infrastructure Partners’ 1,500 MW Murchison Green Hydrogen Project in Western Australia under the Hydrogen Headstart Program. The project, powered by 1.2 GW of solar and 1.7 GW of wind energy, aims to produce renewable hydrogen and ammonia entirely off-grid, with a production capacity of up to 3,600 tonnes per day of ammonia.

• New Hydrogen Production Tax Incentive Unveiled: In May 2024, the Australian government unveiled a new Hydrogen Production Tax Incentive (HPTI) that would pay developers AUD 2 (USD 1.32) per kilo of green hydrogen throughout ten years beginning in 2027. This significantly reduces early-stage project risk and bridges the cost gap between green and fossil-derived hydrogen.

• Japanese Investment Flows into Queensland: On January 28, 2025, Japanese energy company ENEOS announced an AUD 200 million investment in a green hydrogen demonstration plant in Queensland. The project, supported by the Queensland and Australian Governments, will produce hydrogen using renewable energy and aims to export it to Japan in methylcyclohexane (MCH) form, strengthening Australia-Japan clean energy collaboration.

• Central Queensland Hydrogen Project Moves Forward: In 2024, a global consortium including Iwatani Corporation, Keppel, Stanwell Corporation, and Marubeni Corporation committed AUD 117 Million to the Central Queensland Hydrogen Project (CQ-H2), targeting production of 200 tonnes per day by 2029 and 800 tonnes per day by 2031 using renewable energy.

• PEM Electrolyzers Lead Technology: Proton Exchange Membrane (PEM) electrolyzers represent a leading technology segment due to their rapid response times and compatibility with intermittent renewable energy sources like solar and wind, which are abundant across Australia.

Request a Business Sample Report for Procurement & Investment Evaluation:

https://www.imarcgroup.com/australia-green-hydrogen-market/requestsample

Key Trends Shaping the Australia Green Hydrogen Market

• Regulatory Enablement and Institutional Support: The market is actively shaped by a structured and coordinated policy environment. Federal and state governments have introduced dedicated hydrogen roadmaps outlining measurable objectives, with an emphasis on early infrastructure rollout, investment attraction, and technology development. Targeted funding programs support feasibility studies, demonstration projects, and electrolyzer installations, while public sector financial institutions extend concessional finance and credit enhancements to mitigate early-stage risk. The new Hydrogen Production Tax Incentive paying AUD 2 per kilo for ten years beginning 2027 is a game-changer for project economics.

• Export-Focused Strategy and International Alignment: Australia is pursuing long-term trade partnerships with Japan, South Korea, and the European Union, all of which are adopting hydrogen import strategies. The country’s export strategy involves developing port-based hydrogen hubs integrated with dedicated renewable energy generation, electrolyzer facilities, and storage infrastructure. Strategic collaboration with foreign governments and energy companies to co-develop production projects, establish shared technical standards, and ensure future offtake is providing a major boost to market growth. This approach draws from Australia’s experience as a global LNG exporter.

• Abundance of Land for Large-Scale Projects: Australia’s widespread land area and sparse population offer a singular benefit for scaling up green hydrogen production. Vast areas of sparsely populated or arid land-including the Pilbara in Western Australia, Eyre Peninsula in South Australia, and central Queensland-are available for building solar farms, wind farms, and electrolyser plants. These areas have high solar irradiance and stable wind regimes optimal for long-duration renewable energy production, enabling Australia to accommodate mega-scale hydrogen projects for both domestic and export markets.

• Existing Energy Infrastructure Integration: Australia’s mature energy infrastructure and established export capacity offer a robust foundation. Major ports like Gladstone, Darwin, and Port Kembla are being upgraded for dual-use so hydrogen or ammonia can be transported economically overseas. High-voltage transmission networks and gas pipeline infrastructure can be upgraded for hydrogen blending or exclusive transport. This flexibility shortens project timelines and reduces entry costs compared to international competitors.

• Industrial Decarbonization Driving Domestic Demand: Steel production, refining, and chemical processing in Gladstone, Kwinana, and the Port of Brisbane are considering green hydrogen for process heat, feedstock replacement, and low-carbon fuel opportunities. Transport operators, especially in mining and freight, are testing hydrogen fuel cell trucks, trains, and equipment. Renewable hydrogen-powered mining trucks tested in Pilbara iron ore operations provide real-world validation of the technology in extreme conditions.

Market Growth Drivers

Abundance of Land and Low Population Density for Large-Scale Projects

Australia’s widespread land area and sparse population offer a singular benefit for scaling up green hydrogen production via massive renewable projects. In contrast to other nations beset by land shortage or local opposition, Australia has access to vast areas of sparsely populated or arid land-including the Pilbara in Western Australia, Eyre Peninsula in South Australia, and central Queensland-for building solar farms, wind farms, and electrolyser plants. These areas have high solar irradiance and stable wind regimes, optimal for long-duration renewable energy production. With less land-use conflict and lower installation costs, Australia can accommodate mega-scale hydrogen projects that can supply both domestic and overseas export markets. The potential to co-locate energy production and hydrogen production facilities minimizes transmission losses and infrastructure costs. This geographical and demographic position enables faster project development and long-term competitiveness in the global green hydrogen supply chain.

Existing Energy Infrastructure and Export Facilities Integration

Australia’s mature energy infrastructure and established export capacity offer a robust foundation for green hydrogen market growth. Australia has decades of experience exporting energy commodities like LNG, and much of the same port facilities, transport logistics, and regulatory structures can be repurposed for hydrogen exports. Major ports like Gladstone, Darwin, and Port Kembla are being upgraded or designed for dual-use so hydrogen-either pure or as ammonia-can be transported economically to overseas markets. Australia’s high-voltage transmission networks and gas pipeline infrastructure, particularly in industrial areas, can be upgraded for hydrogen blending or exclusive hydrogen transport. This flexibility shortens project timelines and reduces the amount of completely new infrastructure required, lowering entry costs for investors and making the path to market faster. By building on existing assets, Australia can build its hydrogen vision more quickly and cheaply than many international competitors.

Government Support Through Tax Incentives and Funding

The Australian national government plays a leading role through comprehensive policies and strategic plans to make Australia a global hydrogen leader. The government identified hydrogen’s ability to stimulate economic growth and lower carbon emissions, developing national strategies that set firm targets for hydrogen production, export, and domestic use. The new Hydrogen Production Tax Incentive paying AUD 2 per kilo of green hydrogen for ten years beginning in 2027 directly bridges the cost gap with fossil-derived hydrogen. ARENA’s $814 million conditional funding for the Murchison project under the Hydrogen Headstart Program demonstrates the scale of government commitment. State governments complement federal initiatives by adapting strategies to their specific renewable resources and industrial bases, creating a multi-level system that fosters innovation and lowers investment risk.

Market Segmentation

IMARC Group provides an analysis of the key trends in each segment of the Australia green hydrogen market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on technology, application, distribution channel, and region.

By Technology:

• Proton Exchange Membrane Electrolyzer

• Alkaline Electrolyzer

• Others

By Application:

• Power Generation

• Transport

• Others

By Distribution Channel:

• Pipeline

• Cargo

By Region:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & South Australia

• Western Australia

Key Players

The competitive landscape features a mix of domestic developers and international technology providers. Key players analyzed include ABEL Energy Pty Ltd, Allied Green Ammonia, Edify Energy Pty Ltd, Hysata, LINE Hydrogen, Nel Hydrogen, Star Scientific Limited, and Yarra Valley Water. The report provides a comprehensive analysis of the competitive landscape including key player positioning, market structure, and winning strategies.

Key Aspects Required for the Australia Green Hydrogen Market

• PEM Electrolyzers Lead Technology: Proton Exchange Membrane (PEM) electrolyzers are the leading technology segment due to their rapid response times and compatibility with intermittent renewable energy sources like solar and wind. Alkaline electrolyzers remain important for steady-state, continuous operation, while emerging technologies are being piloted for efficiency improvements.

• Cargo (Shipping) Is Critical Distribution Channel: Given Australia’s export focus to Asian markets like Japan and South Korea, cargo shipping is the dominant distribution channel. Hydrogen is typically converted to ammonia or carried in liquid organic hydrogen carriers like MCH for cost-effective transport, with major ports (Gladstone, Darwin, Port Kembla, Dampier) being upgraded for this purpose.

• Power Generation and Transport Key Applications: Power generation uses hydrogen for grid stability and long-duration storage, including hydrogen-fired turbines and blending into natural gas networks. Transport applications include hydrogen fuel cell trucks, trains, mining equipment, and buses, with Pilbara iron ore operations testing hydrogen-powered mining trucks in extreme conditions.

• Western Australia Leads Regional Development: Western Australia is the frontrunner due to its world-class solar and wind resources in the Pilbara and Mid-West regions, existing port infrastructure, and the massive Murchison project. Queensland is also advancing rapidly with the CQ-H2 project and ENEOS investment. South Australia is leveraging its wind resources for hydrogen production, while NSW focuses on port-based export hubs.

• Hydrogen Production Tax Incentive Makes Economics Work: The HPTI paying AUD 2 per kilo of green hydrogen for ten years from 2027 fundamentally changes project economics. This production credit directly bridges the cost gap with grey hydrogen and gives Australian projects a competitive advantage in Asian export markets.

• Ammonia Export Is Near-Term Pathway: Most near-term export projects plan to convert hydrogen to ammonia for easier shipping, then c r a c k it back to hydrogen or use directly in ammonia-based applications (fertilizer, power generation co-firing). The Murchison project targets up to 3,600 tonnes per day of ammonia production.

• International Partnerships Secure Offtake: Australia is actively signing MOUs and investment agreements with Japanese (ENEOS, Iwatani, Marubeni), South Korean, and European partners. These partnerships not only bring capital but secure long-term offtake agreements that make final investment decisions possible for multi-billion-dollar projects.

• Water Availability Is a Challenge for Arid Regions: Electrolysis requires significant water inputs, which is challenging in arid regions like the Pilbara where many hydrogen projects are planned. Projects are investing in water-efficient electrolysis technologies, desalination plants, and water recycling to address this constraint.

Recent News and Developments

• April 22, 2025: Adani Ports purchased Australia’s NQXT terminal, enhancing its cargo capacity by 35 million tons and elevating EBITDA, as it aims to hit 1 Billion Tons each year by 2030. The AUD 3.975 Billion agreement is a non-cash equity exchange that expands Adani’s international logistics presence, with opportunities for green hydrogen exports.

• March 20, 2025: ARENA announced $814 Million in conditional funding for Copenhagen Infrastructure Partners’ 1,500 MW Murchison Green Hydrogen Project in Western Australia under the Hydrogen Headstart Program. The project, powered by 1.2 GW of solar and 1.7 GW of wind energy, aims to produce renewable hydrogen and ammonia entirely off-grid, with a production capacity of up to 3,600 tonnes per day of ammonia.

• January 28, 2025: Japanese energy company ENEOS announced an AUD 200 million investment in a green hydrogen demonstration plant in Queensland, Australia. The project, supported by the Queensland and Australian Governments, will produce hydrogen using renewable energy and aims to export it to Japan in methylcyclohexane (MCH) form.

• January 10, 2024: Australia selected six major electrolysis projects for a A2bn(US2bn(US1.34bn) initiative aimed at reducing carbon emissions in heavy industry and establishing itself as a frontrunner in green hydrogen production and export. The chosen projects comprise the 1,625 MW Murchison initiative in Western Australia and the 750 MW Kepco Australia plant at the Port of Newcastle in New South Wales.

• May 2024: The Australian government unveiled a new Hydrogen Production Tax Incentive (HPTI) that would pay developers AUD 2 (USD 1.32) per kilo of green hydrogen throughout ten years beginning in 2027.

• 2024: A global consortium including Iwatani Corporation, Keppel, Stanwell Corporation, and Marubeni Corporation committed AUD 117 Million to the Central Queensland Hydrogen Project (CQ-H2), targeting production of 200 tonnes per day by 2029 and 800 tonnes per day by 2031 using renewable energy.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=34626&flag=E

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel. No.: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.