Europe Hydrogen Generator Market Report Summary

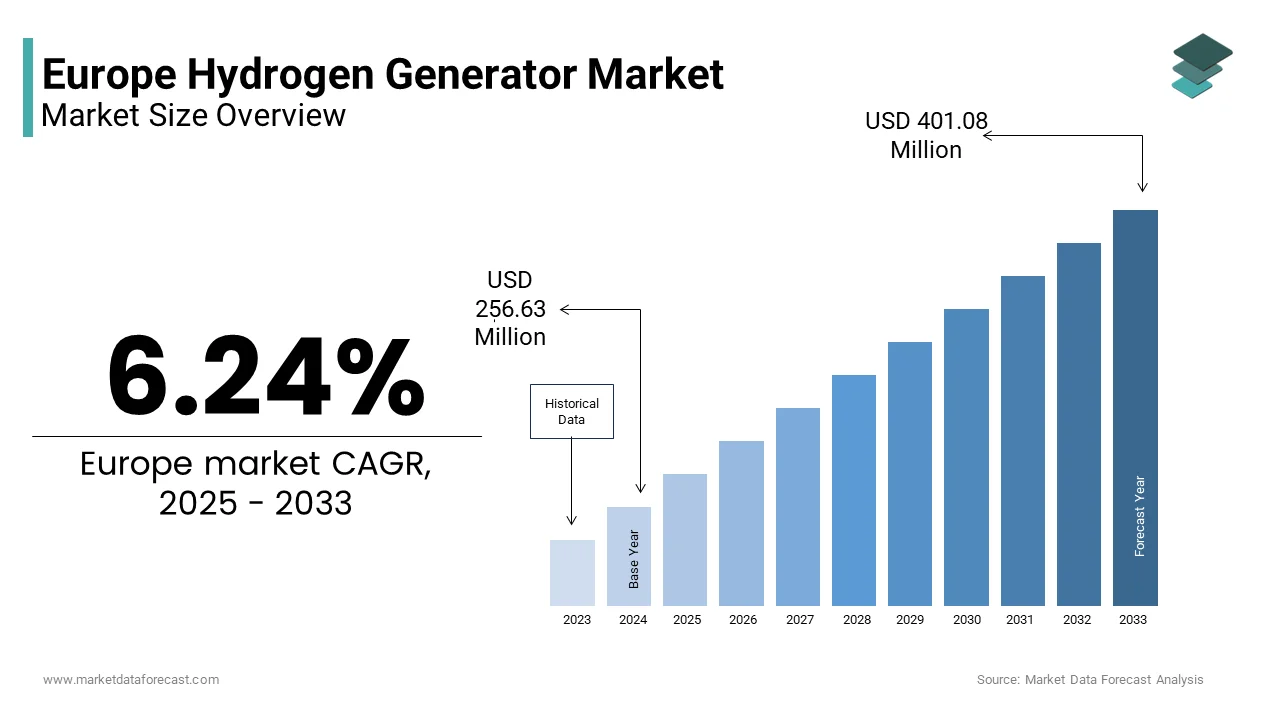

The Europe hydrogen generator market was valued at USD 241.52 million in 2024, is estimated to reach USD 256.63 million in 2025, and is projected to reach USD 401.08 million by 2033, growing at a CAGR of 6.24% during the forecast period from 2025 to 2033.

Market growth is driven by Europe’s strong commitment to clean energy transition, rapid expansion of the green hydrogen economy, and increasing deployment of on-site hydrogen generation systems across industrial sectors. Supportive EU policies, advancements in electrolysis and reforming technologies, and growing investment in hydrogen infrastructure are further propelling market adoption.

KEY MARKET TRENDS

- Rising adoption of hydrogen as a clean energy source in refineries, chemical plants, and mobility sectors, driven by the EU’s 2050 carbon neutrality target.

- Expansion of green hydrogen initiatives through large-scale electrolysis projects and renewable-powered generation plants.

- Advancements in reforming and electrolysis technologies are improving cost efficiency, purity levels, and operational flexibility of hydrogen generation systems.

- Industrial decarbonization programs are encouraging the replacement of conventional hydrogen supply chains with distributed, on-site production models.

- Strategic partnerships and pilot projects among energy companies, technology providers, and governments to accelerate Europe’s hydrogen infrastructure build-out.

SEGMENTAL INSIGHTS

- By Production Technology: The steam methane reforming (SMR) segment led the Europe hydrogen generator market in 2024, capturing a 61.4% share. Despite the rising focus on green hydrogen, SMR remains the dominant technology due to its cost-effectiveness, established infrastructure, and ability to support large-scale industrial hydrogen production.

- By Application: The oil refining segment held the largest market share at 34.7% in 2024, driven by the increasing need for hydrogen in desulfurization and hydrocracking processes. Refineries continue to expand hydrogen generation capacity to meet stricter fuel quality standards and emissions targets across Europe.

REGIONAL INSIGHTS

- Germany dominated the Europe hydrogen generator market in 2024, accounting for a 24.6% share, backed by robust renewable investments, government incentives, and integration of hydrogen into industrial clusters and mobility systems.

- France followed with a 16.8% share, propelled by its national hydrogen roadmap emphasizing decarbonization of heavy industries and energy storage solutions.

- The Netherlands continues to hold a significant position as a hydrogen logistics and transport hub for Northwest Europe, benefiting from its advanced port infrastructure and cross-border energy collaborations.

COMPETITIVE LANDSCAPE

The European hydrogen generator market is characterized by a mix of global energy giants and regional innovators focusing on green hydrogen production, electrolysis technologies, and scalable modular systems. Key players are prioritizing cost optimization, renewable integration, and large-scale deployment through partnerships and pilot programs.

Prominent companies in the Europe hydrogen generator market include Linde plc, ThyssenKrupp Nucera, Nel ASA, ITM Power, Air Liquide, Messer Group GmbH, Plug Power Inc., Engie SA, Nikola Corporation, Air Products & Chemicals Inc., FuelCell Energy Inc., and Enapter AG.

Europe Hydrogen Generator Market Size

The hydrogen generator market size was valued at USD 241.52 million in 2024 and is anticipated to reach USD 256.63 million in 2025 to USD 401.08 million by 2033, growing at a CAGR of 6.24% during the forecast period from 2025 to 2033.

A hydrogen generator is a device that produces hydrogen gas, which can be used as an energy source or for industrial applications. Unlike global markets dominated by grey hydrogen from fossil sources, Europe’s focus is decisively on low-carbon and renewable-based generation aligned with its net-zero ambition. According to an International Energy Agency (IEA) 2024 report, global announced electrolyzer capacity that has reached a final investment decision (FID) stands at 20 GW, with projects using electrolysis driving most of the growth in low-emissions hydrogen production. The EU has adopted delegated acts since 2023 with rules to define renewable hydrogen and has launched auctions through the European Hydrogen Bank to support projects. As per the European Hydrogen Observatory, hydrogen demand in the EU in 2023 was estimated at 7.93 Mt, mainly used in refineries and the ammonia industry. Furthermore, the Critical Raw Materials Act designates iridium and platinum, key catalysts in electrolysis, as strategic inputs. This regulatory and technological ecosystem positions hydrogen generators not as peripheral equipment but as core enablers of Europe’s industrial decarbonization and energy sovereignty strategy.

MARKET DRIVERS

EU Green Deal Mandates for Industrial Decarbonization

The European Green Deal’s binding decarbonization targets are compelling heavy industries to replace fossil-derived hydrogen with on-site low carbon generation, a shift that is fuelling the growth of the Europe hydrogen generator market. According to studies, regulatory frameworks like the European Commission’s Carbon Border Adjustment Mechanism are increasingly requiring the reporting of embedded emissions from hydrogen use in industrial sectors, which indicates a trend toward stricter enforcement and financial accountability. This has accelerated the adoption of electrolytic hydrogen in sectors where hydrogen is a feedstock rather than a fuel. In response to regulatory targets, a significant portion of the chemical industry is piloting on-site low-carbon hydrogen production technologies. Similarly, the steel sector, through initiatives, plans to eliminate coking coal using green hydrogen produced via megawatt-scale generators. This policy-driven transition transforms hydrogen generators from optional assets into compliance necessities for Europe’s industrial core.

Expansion of Renewable Energy Integration for Grid Balancing

The need to stabilize the region’s electricity grid amid soaring renewable penetration is driving the expansion of the Europe hydrogen generator market. This is caused by flexible demand side assets that convert surplus wind and solar power into storable hydrogen. According to studies, Renewable energy sources are increasingly contributing a larger share to the European Union’s electricity generation mix, though this growth is accompanied by a rise in instances where renewable output must be limited due to constraints within the electricity grid. Hydrogen electrolyzers offer a dispatchable load that absorbs excess power during peak generation periods, thereby reducing waste and enhancing grid resilience. As per research, operators of electrolyzer plants in certain regions are adopting more flexible and dynamic operational modes, which have proven effective in mitigating the need to curtail renewable energy generation in those areas. National energy and climate plans in some countries are establishing significant mandates for the development of electrolysis capacity, specifically designating this capacity to support the integration of renewable energy into the power system. This dual value proposition, energy storage and grid service, elevates hydrogen generators from production tools to strategic grid infrastructure, re-accelerating their adoption beyond traditional industrial users.

MARKET RESTRAINTS

High Capital and Operational Costs of Electrolyzer Systems

The substantial upfront investment and energy intensity of these generators remain major restraints to the Europe hydrogen generator market. According to recent International Energy Agency (IEA) reports, the installed cost of electrolysers outside of China in 2024 ranged from $2,000 to $2,600 per kilowatt, while systems in China were considerably cheaper (around $750-$1,300/kW). For a typical 1-megawatt system, this translates to €1 million or more in initial outlay. Operational costs are further burdened by electricity prices. As per a 2024 report of the European Court of Auditors (ECA), the EU’s hydrogen production and import targets for 2030 are unlikely to be met, and there are significant challenges, including a lack of guaranteed demand (offtakers) and an uncertain price environment, which hinder the long-term financial sustainability of many projects beyond initial grant support. Moreover, maintenance of membrane catalysts and cooling systems requires specialized technicians, a workforce in short supply across the EU. The economic case for hydrogen generators will only be solid for the largest industrial players once capital costs are reduced through scaling and electricity prices are stabilized via dedicated renewable power purchase agreements (PPAs).

Insufficient High-Purity Water Infrastructure for Electrolysis

The lack of reliable infrastructure for supplying the ultra-pure deionized water required for electrolysis, especially in water-stressed regions, restrains the expansion of the Europe hydrogen generator market. Proton exchange membrane (PEM) electrolyzers utilize high-purity water and have a consistent water consumption rate kilograms of hydrogen produced. According to research, a significant number of European Union member states, particularly in Southern Europe, are experiencing substantial water stress and groundwater depletion. As per sources, freshwater consumption concerns are a primary cause of permitting delays for many planned electrolyzer projects in Southern Europe. In response, some regions are beginning to mandate closed-loop water recycling for hydrogen production facilities, which increases the initial capital investment required for these projects. The European Commission’s Water Resilience Strategy acknowledges this barrier and calls for integration of desalination and wastewater reuse, but implementation lags. The expansion of on-site hydrogen generation might be limited by the simple lack of available water resources, rather than by technological or political issues, if we fail to plan for the coordinated management of water and hydrogen systems.

MARKET OPPORTUNITIES

Deployment of Hydrogen Generators in Semiconductor Manufacturing Clusters

The rapid expansion of the region’s semiconductor industry is providing a key opportunity for the Europe hydrogen generator market. This is due to the sector’s stringent purity and continuity requirements. According to sources, the European Union is actively working to significantly increase its share of the global semiconductor market within the next decade, supported by substantial investment in the construction of new fabrication plants across several member nations. These fabs require a continuous supply of pure hydrogen for wafer annealing and chemical vapor deposition; any interruption risks million-euro wafer losses. As per research, On-site hydrogen generation solutions, specifically electrolysis, are becoming the preferred option in the European semiconductor industry because of the safety risks and purity challenges linked to bulk transport. Companies within the industry have already begun the process of adopting and installing modular on-site hydrogen generation systems to meet their operational needs. European Union initiatives and programs are encouraging the integration of on-site hydrogen generators as a recognized and fundable investment within new chip manufacturing projects. This convergence of strategic industrial policy and technical necessity positions semiconductor clusters as early adopters and innovation hubs for next-generation hydrogen generation systems tailored to ultra-high purity industrial demand.

Integration with Offshore Wind Power Hubs in the North Sea

The co-location of hydrogen generators with offshore wind farms in the North Sea introduces a potential prospect for the expansion of the Europe hydrogen generator market. This offers an opportunity to produce green hydrogen at scale while bypassing onshore grid constraints. According to studies, Multiple European nations are collaborating to substantially increase offshore wind capacity by 2030, integrating this with dedicated offshore hydrogen production facilities. Demonstration projects are successfully testing the use of excess (curtailed) offshore wind power to produce hydrogen via electrolysis, with plans for transport to shore via pipelines. Similarly, national-level agreements in Europe are setting specific capacity targets and allocating sea areas for large-scale offshore hydrogen production within the current decade. This model eliminates expensive grid reinforcement and reduces transmission losses, which can increase long-distance electricity transport. European Union policy and strategy are actively promoting the development of the offshore renewable energy sector, including supporting the infrastructure needed for cross-border hydrogen transport. The industry anticipates that scaling up this maritime approach, with commercial-scale offshore electrolyzers expected soon, will lead to significant reductions in the cost of producing hydrogen. Europe’s maritime advantage can be fully realized by developing wind-rich coasts into green hydrogen export hubs, positioning the continent as a leader in deploying power generation technology and spearheading clean energy initiatives on the world stage.

MARKET CHALLENGES

Intermittent Renewable Supply and Electrolyzer Degradation

The variable output of the region’s dominant renewable sources, wind and solar, poses a challenge to the Europe hydrogen generator market. This affects operational longevity and efficiency of hydrogen generators. Electrolyzers are designed for stable load conditions, yet frequent start-stop cycles and partial load operation, common in grid-connected renewable environments, accelerate degradation of membranes and catalysts. This performance gap increases the total cost of ownership and complicates bankability assessments for investors. Compounding the issue is the lack of standardized protocols for testing electrolyzer durability under variable conditions. Widespread technical and economic constraints will continue to hinder the promise of low-cost green hydrogen until we see the mainstream adoption of robust control systems and degradation-resistant materials.

Lack of Harmonized Certification for On-Site Hydrogen Quality

The absence of a unified European standard for certifying the purity and safety of hydrogen produced by on-site generators creates regulatory uncertainty and hinders cross-border adoption, which in turn inhibits the expansion of the Europe hydrogen generator market. The quality requirements for hydrogen vary significantly across different industrial sectors, with specific industries like pharmaceuticals, electronics, and food processing often needing stricter purity thresholds than those defined by general mobility standards like ISO 14687. Moreover, the lack of real-time monitoring mandates means impurities like oxygen or moisture may go undetected until process failures occur. The absence of a common EU-wide certification framework for electrolytic hydrogen generators will fragment the market, resulting in redundant testing costs and slow project approvals, which in turn hinders the necessary scale for industrial change and cost efficiencies.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2023 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.24% |

|

Segments Covered |

By Type, Production Technology, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden |

|

Market Leaders Profiled |

Linde plc, Air Liquide, Messer Group GmbH, Plug Power Inc., Engie SA, Nikola Corporation, Air Products & Chemicals Inc., FuelCell Energy Inc., Enapter AG |

SEGMENTAL ANALYSIS

By Type Insights

The grey hydrogen segment remained dominant in the Europe hydrogen generator market and accounted for a 58.2% share in 2024. The dominance of the grey hydrogen segment is attributed to entrenched infrastructure and cost advantages in existing industrial operations. Most hydrogen generators in refineries and ammonia plants still rely on steam methane reforming of natural gas without carbon capture, a legacy system that benefits from decades of optimization and low capital replacement urgency. Transitional policy tolerance is another key accelerator of this segment. This regulatory grace period allows sectors like oil refining, where hydrogen is essential for desulfurization, to delay costly retrofits. The current dominance of grey hydrogen, a result of established infrastructure and lower costs, is set to continue unless either green hydrogen achieves cost competitiveness or a carbon price exceeding €100/tonne is implemented.

The green hydrogen segment is anticipated to witness the fastest CAGR of 47.3% from 2025 to 2033 due to binding EU decarbonization mandates and targeted public investment. According to sources, green hydrogen production in the EU grew largely fueled by electrolyzer deployments in Germany, Spain, and the Netherlands. A further driver of this segment is Corporate procurement. Crucia,lly the EU’s Carbon Border Adjustment Mechanism indirectly penalizes grey hydrogen use by increasing the embedded carbon cost of imported steel and chemicals, which accelerates internal shifts toward electrolytic generation. Electrolyzer manufacturing capacity in Europe is expected to increase in the coming years. So, green hydrogen is transitioning from pilot phase to industrial scale at an unprecedented speed.

By Production Technology Insights

The steam methane reforming segment led the Europe hydrogen generator market and captured a 61.4% share in 2024. Factors such as its maturity, reliability, and integration with existing natural gas infrastructure across industrial clusters contribute significantly to the prominence of the steam methane reforming segment. Most of Europe’s ammonia and methanol plants currently rely on SMR-based hydrogen production units. According to sources, SMR-based hydrogen generation is significantly more cost-effective than electrolytic alternatives. Transitional compatibility with blue hydrogen pathways also propels the growth of this segment. As per sources, a number of large-scale SMR projects in several European countries have been upgraded with carbon capture technology, which significantly reduces their CO₂ emissions. This hybrid approach allows industries to decarbonize incrementally without abandoning sunk capital. SMR is projected to remain the primary source of hydrogen until a future date when the costs of electrolyzers and renewable electricity decrease substantially.

The electrolysis segment is likely to experience the fastest CAGR of 45.8% during the forecast period, owing to policy mandates and renewable energy integration imperatives. The European Union’s delegated act on renewable hydrogen requires that all electrolytic hydrogen used for compliance purposes must be produced using additionality and temporal correlation principles, which effectively links generators directly to new wind and solar assets. A different growth driver of this segment is industry-off-take certainty. Moreover, the Critical Raw Materials Act supports domestic production of iridium and nickel catalysts, reducing supply chain risks. These converging factors position electrolysis not as a future possibility but as the present engine of Europe’s clean hydrogen industrial policy.

By Application Insights

The oil refining segment was the largest in the Europe hydrogen generator market and occupied a 34.7% share in 2024. The growth of the refining segment is driven by the sector’s structural dependence on hydrogen for hydrodesulfurization and hydrocracking processes mandated by EU fuel quality standards. Refineries throughout the European Union consistently need a small amount of hydrogen during production processes to ensure diesel meets environmental regulations, specifically regarding the reduction of sulfur content. This regulatory requirement across numerous refineries results in a substantial annual demand for hydrogen within the EU. Operational continuity further propels the growth of this segment. This regulatory and operational lock-in ensures oil refining remains the bedrock of hydrogen generator demand through the late 2020s.

The iron and steel production segment is on the rise and is expected to be the fastest-growing segment in the global market by witnessing a CAGR of 52.1% from 2025 to 2033 due to factors such as the complete reengineering of steelmaking around direct reduced iron using green hydrogen. The European steel industry is projected to transition a significant portion of its production to hydrogen-based processes due to the impact of rising carbon pricing regulations. According to studies, pilot programs in the steel industry have successfully demonstrated substantial reductions in carbon dioxide emissions by substituting traditional coking coal with electrolytic hydrogen. Public funding is also among the key accelerators of this segment. These projects require multi-megawatt electrolyzers operating 24 hours a day, which creates unprecedented demand intensity. The EU steel sector, a significant source of the region’s industrial emissions, must transition to hydrogen-based production to survive the impact of impending CBAM tariffs on exports.

COUNTRY ANALYSIS

Germany Hydrogen Generator Market Analysis

Germany outperformed other countries in the Europe hydrogen generator market by accounting for a 24.6% share in 2024. The domination of Germany in the regional market is propelled by its industrial base, strong policy framework, and leadership in green steel and chemicals. It is implementing significant national strategies and providing substantial public funding to rapidly expand its domestic electrolysis capacity. According to sources, there is substantial progress in developing large-scale hydrogen generator projects across Germany, with numerous high-capacity facilities currently under construction. Integrated hydrogen production systems, combining different technologies, are being established in key industrial regions to supply major corporations. Germany is pursuing international partnerships and import initiatives to supplement its domestic green hydrogen supply. A combination of stringent carbon pricing and binding renewable hydrogen quotas under the Renewable Energy Sources Act allows Germany to apply regulatory pressure and achieve industrial scale, thereby driving sustained market dominance.

France Hydrogen Generator Market Analysis

France is the next-biggest player in the Europe hydrogen generator market by capturing a 16.8% share in 2024. State-led investment in nuclear-powered electrolysis and sovereign industrial decarbonization are the factors fuelling the growth of the French market. It allocates notable funds to develop low-carbon hydrogen with a unique focus on using nuclear energy for stable baseload electrolysis. The country also leads in hydrogen mobility with numerous refueling stations and mandates for green hydrogen in fertilizer production. France’s emphasis on energy independence and technological sovereignty, exemplified by its exclusion of foreign electrolyzer vendors from critical projects, positions it as a distinct model where hydrogen generation aligns with national strategic autonomy.

Netherlands Hydrogen Generator Market Analysis

The Netherlands continues to maintain a notable share in the Europe hydrogen generator market, with its role as a European hydrogen logistics hub and concentration of petrochemical complexes in the Port of Rotterdam. The country’s extensive natural gas pipeline network is being repurposed for hydrogen transport under the national Hydrogen Backbone plan, which will connect industrial sites in the coming years. The Netherlands also pioneers cross-border hydrogen trade. This combination of infrastructure readiness, industrial clustering, and international connectivity makes the Netherlands a pivotal node in Europe’s emerging hydrogen economy.

Sweden Hydrogen Generator Market Analysis

Sweden is expected to be the most lucrative region in the Europe hydrogen generator market due to its pioneering role in fossil-free steel and abundant renewable electricity. The country generates a notable share of its power from hydroelectric sources and from nuclear, which provides low-cost cost clean electricity ideal for electrolysis. According to the Swedish Energy Agency (SEA), the proposed national target for electrolyzer capacity is 5 gigawatts (GW) by 2030. The government’s Fossil Free Sweden initiative provides tax exemptions and fast-track permitting for green hydrogen projects. Sweden’s core industries, iron ore mining and steelmaking, drive its use of hydrogen generators, which creates global export competitiveness in green materials rather than just meeting regulatory compliance.

Spain Hydrogen Generator Market Analysis

Spain is predicted to grow in the Europe hydrogen generator market between 2025 and 20233 owing to its exceptional solar and wind resources and strategic positioning as a green hydrogen exporter to North Africa and Central Europe. According to the Spanish Ministry for Ecological Transition and grid operators, over 100 gigawatts of renewable project applications linked to future hydrogen production have been submitted for grid access, with a significant but unconfirmed portion (around 40 GW) in Andalusia. The updated National Integrated Energy and Climate Plan (PNIE, C), approved in September 2024 (and in its draft form in June 2023), actually targets 12 gigawatts (GW) of electrolysis capacity by 2030, which is an increase from the previous 4 GW target. Spain is poised to become a core hydrogen generator for the European continent, leveraging its low land costs, high renewable yields, and strong political backing to move beyond its role as a peripheral energy consumer.

COMPETITIVE LANDSCAPE

Competition in the Europe hydrogen generator market is intensifying as a blend of established industrial engineering firms, specialized electrolyzer startups, and global energy majors vie for leadership in the policy-driven, emerging sector. Unlike mature markets, where price and performance dominate, Europe’s competitive landscape is shaped by compliance with the EU’s Net Zero Industry Act local content rules and eligibility for Innovation Fund grants. Companies must demonstrate secure supply chains for critical raw materials, robust recycling pathways, and integration with renewable energy sources to qualify for public support. This regulatory complexity favors firms with strong European manufacturing presence and deep industrial partnerships. At the same time, technological divergence between alkaline and proton exchange membrane electrolysis creates parallel innovation tracks with different co, st durability, and scalability profiles. The market is further fragmented by national hydrogen strategies that prioritize domestic champions such as Nel in Norway and ThyssenKrupp Nucera in Germany. As a result, competitive advantage stems not from global scale alone but from regional embeddedness, policy fluency, and the ability to deliver bankable integrated solutions that satisfy Europe’s unique decarbonization imperative.

KEY MARKET PLAYERS

A few of the market players in the Europe hydrogen generator market include

- Linde plc

- ThyssenKrupp nucera

- Nel ASA

- ITM Power

- Air Liquide

- Messer Group GmbH

- Plug Power Inc.

- Engie SA

- Nikola Corporation

- Air Products & Chemicals Inc.

- FuelCell Energy Inc.

- Enapter AG

Top Players In The Market

- Nel ASA is a leading European provider of hydrogen generators with a strong global footprint in proton exchange membrane and alkaline electrolysis technologies. Headquartered in Norway, the company supplies modular and megawatt-scale systems to industrial and energy customers across Europe, North America, and Asia. Nel has significantly advanced Europe’s hydrogen infrastructure by delivering electrolyzers for landmark projects, including the NortH2 consortium in the Netherlands and the H2Haul initiative in Germany. These actions reinforce Nel’s role in accelerating cost-competitive and scalable green hydrogen production aligned with EU decarbonization goals.

- ThyssenKrupp Nucera plays a pivotal role in the Europe hydrogen generator market through its large-scale alkaline electrolysis technology tailored for industrial decarbonization. It has supplied multi-hundred megawatt systems to projects such as the NEOM green hydrogen facility in Saudi Arabia and the ArcelorMittal steel decarbonization program in France. These moves solidify its position as a key enabler of Europe’s industrial hydrogen transition.

- ITM Power contributes to the Europe hydrogen generator market through its high-efficiency proton exchange membrane electrolyzers designed for dynamic operation with renewable energy. Based in the United Kingdom, the company has deployed systems across Germany, Denmark for grid balancing, mobility,, ty and industrial applications. ITM Power pioneered the concept of factory-built modular electrolysis, reducing site construction time and cost. The initiatives enhance ITM Power’s ability to support Europe’s transition to flexible and reliable green hydrogen generation.

Top Strategies Used By The Key Market Participants

Key players in the Europe hydrogen generator market pursue strategies centered on scaling manufacturing capacity, securing critical raw material supply chains, and forming industry off-taker alliances. Companies are investing billions in gigafactories within the EU to localize production and comply with the Net Zero Industry Act’s domestic content requirements. They are developing catalyst technologies that reduce or eliminate dependence on iridium and platinum through partnerships with research institutes under Horizon Europe. Strategic collaborations with steel, chemical ,and energy firms ensure long-term hydrogen offtake and co-development of integrated generation systems. Additionally, firms are standardizing modular designs to enable rapid deployment and participating in EU-funded hydrogen valleys to demonstrate cross-sectoral value chains. These approaches reflect a shift from equipment sales to ecosystem enablement, where success depends on reliability,scalabilityd regulatory alignment.

MARKET SEGMENTATION

This research report on the Europe hydrogen generator market is segmented and sub-segmented into the following categories.

By Type

By Production Technology

- Steam Methane Reforming (SMR)

- Electrolysis

- Others

By Application

- Oil Refining

- Chemical Processing

- Iron and Steel Production

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe