This is an extract from a recent report “FICCI-EY report on innovation and critical technologies” by FICCI and EY.

India’s energy agenda includes ambitious renewable energy targets and a rapidly evolving electric mobility ecosystem. With projected power demand expected to rise to 708 GW by 2047, necessitating a fourfold increase in installed capacity to 2,100 GW requires a balance between meeting higher demand with sustainability goals. India’s clean energy transition strategy therefore encompasses renewable energy expansion, green hydrogen capacities and electric vehicle adoption.

The Central Electricity Authority’s National Electricity Plan 2022-32 projects a consistent upward trend in peak electricity demand, with projections rising from 203,115 MW in 2021-22 to 366,393 MW in 2031-32 (CAGR of 6.1%). This growing demand, coupled with India’s commitment to achieving 500 GW of renewable capacity by 2030 necessitates a fundamental restructuring of the energy infrastructure and economic model.

Solar energy: Harnessing India’s natural advantage

Solar energy: Harnessing India’s natural advantage

Harnessing India’s natural advantage. With 300 days of sunshine annually and solar irradiance ranging from 4-7 kWh/m²/day, India receives 2,300-3,200 sunshine hours annually, offering an estimated potential of 5,000 BU of electricity per year or approximately 2,500 GW of capacity at current efficiency levels (CGIAR Research).

The solar sector has demonstrated remarkable growth over the past decade, with installed capacity growing at a CAGR of 36.5% over the past 11 years, as per an EY report on energy transition. This reflects India’s role in the global solar energy transition, supported by government policies and increasing uptake of solar projects across various sectors.

India’s National Electricity Plan aligns with the country’s commitment to the Paris Agreement and outlines an ambitious roadmap targeting 280 GW of solar power capacity by 2030 as part of the broader 500 GW renewable energy target, as per a government announcement. This solar capacity expansion is supported by several key government initiatives that have proven instrumental in driving sector growth.

Solar Parks and Ultra Mega Solar Power Projects, initiated in 2014, established the foundation for large-scale solar deployment, creating dedicated infrastructure zones that enabled efficient land acquisition, grid connectivity, and project development processes, significantly reducing the complexity and cost of solar installations.

The PM Surya Ghar Muft Bijli Yojana, launched in 2024, along with the Pradhan Mantri Suryoday Yojana, has given momentum to the target of 10 million household rooftop solar installations, democratizing access to solar energy and reducing transmission losses through distributed generation.

Wind energy: Capturing India’s atmospheric resources

India ranks fourth worldwide with an installed capacity of 46.42 GW, reflecting the maturing wind technology deployment, as per government data. The government has set an ambitious target of 140 GW renewable capacity from wind by 2030, including 30 GW from offshore wind development. In 2023 alone, India commissioned over 2.8 GW of onshore wind capacity, demonstrating consistent progress toward these targets despite global supply chain challenges and technological transitions, as per government data. The 2023 National Repowering Policy represents a significant strategic initiative aimed at modernizing aging wind turbines and enhancing overall sector efficiency.

Offshore wind development is the next frontier. The government’s 4 GW seabed leasing plan, backed by INR 7,453 crore in Viability Gap Funding, aims to accelerate capacity expansion in offshore areas along India’s extensive coastline. These offshore projects offer higher capacity factors and reduced land acquisition challenges compared to onshore developments.

Infrastructure development in key wind-rich states like Gujarat and Tamil Nadu continues to support sector growth through enhanced transmission connectivity, port facilities for component transportation, and specialized manufacturing zones for wind equipment production.

Battery energy storage and real-time integration

Integration of battery energy storage systems (BESS) with renewable energy projects is important for grid stability and reliability as renewable energy penetration increases. Energy storage investments have risen dramatically from just 1% of deal volume in 2017 to 9% by 2024, with lithium-ion batteries dominating.

BESS support grid flexibility and reliability by allowing frequency regulation, voltage support, peak shaving, and renewable energy time-shifting to address the intermittency challenges in solar and wind generation.

Hybrid systems combine solar, wind and storage components to provide round-the-clock renewable power delivery. These integrated systems can participate in various electricity markets while providing grid services that enhance overall system reliability.

Smart grid integration is the next evolutionary step in battery storage deployment, enabling dynamic response to grid conditions and optimized energy management across distributed generation resources. Advanced battery management systems can coordinate with grid operators to provide real-time balancing services while maximizing economic returns for project operators.

Batteries installed in India post-2024 are projected to be profitable, driven by falling battery storage costs (expected to decline approximately 60% by 2030), rising renewable energy penetration and supportive government tenders under the National Green Hydrogen Mission and renewable integration schemes. Energy Storage Systems (ESS) inclusion in renewable energy tendering has steadily increased from 16% to 43% since 2019.

Green hydrogen: The future fuel economy

Green hydrogen: The future fuel economy

Green hydrogen represents a transformative opportunity for India to reduce its dependence on fossil fuels, largely imported, while positioning itself as a global hub for clean energy exports. The government has allocated US$2.4 billion in subsidies to renewable hydrogen projects through the National Green Hydrogen Mission. For the financial year 2025-26, the Union Budget allocated INR600 crore to the National Green Hydrogen Mission.

The ambitious target of producing 5 MMT (million metric tons) of green hydrogen annually by 2030 requires scaling up industrial capacity, additional 125 GW of dedicated renewable capacity, robust water logistics infrastructure and domestic electrolyzer manufacturing capabilities. Water availability and quality become critical factors in project site selection, particularly in water-stressed regions where competition for water resources could limit project viability. Development of domestic electrolyzer manufacturing capabilities represents both a strategic opportunity and a necessity for India’s green hydrogen ambitions.

The disparity between India’s potential green hydrogen production capacity and domestic consumption creates opportunities for export market development. Currently, 90% of hydrogen consumption in India serves captive purposes, resulting in a relatively small tradeable market that limits economies of scale development.

Until robust domestic demand is established, exporting represents a vital strategy for achieving the economies of scale necessary for cost reduction and technological advancement. The EU, Japan, and South Korea are major import markets due to their aggressive consumption targets and limited domestic production capabilities. There are media reports of several major projects in India securing offtake agreements with international buyers.

India’s green hydrogen sector is rapidly transitioning from pilot projects to global trade collaborations, with large-scale export agreements and industrial tie-ups reinforcing commercial viability and providing revenue certainty for large-scale project development. A proposed 1.2 MTPA green hydrogen and ammonia project has secured an offtake agreement with a corporation in Japan, exemplifying an emerging export model. Another entity has entered into foreign agreements to export green hydrogen. An agreement for renewable ammonia supply has been signed by a production facility, integrating green hydrogen into established chemical value chains.

India could potentially capture 10% of the global green hydrogen market, translating to approximately 10 MMT of green hydrogen and green ammonia exports annually, as per government estimates.

Export opportunities and market development

The fertilizer industry, currently reliant on imported natural gas and ammonia, represents one of the most promising domestic applications for green hydrogen in India. The Ministry of New and Renewable Energy increased the annual production capacity for green ammonia under Mode 2A of the SIGHT scheme from 550,000 to 750,000 tons per year in June 2024. In August 2025, the first SECI auction under Mode 2A resulted in a discovered price of just INR 55.75 per kg, only 10.1% higher than grey ammonia, signaling a potential shift toward greater price parity. Fourteen fertilizer plants identified in the Solar Energy Corporation of India’s tender will consume this green ammonia, creating a guaranteed domestic market for green hydrogen production.

This transition to green ammonia in fertilizer manufacturing supports India’s net-zero vision while reducing import dependency of critical agricultural inputs. The shift could significantly insulate the country from global price volatility in fertilizers and natural gas, enhancing food security and agricultural competitiveness.

Steel production represents another major opportunity for green hydrogen adoption, with several major steel producers exploring hydrogen-based direct reduction processes as alternatives to coal-based production. These industrial applications provide the scale necessary for green hydrogen cost reduction while supporting India’s industrial decarbonization objectives.

Electric vehicless: Transforming India’s mobility landscape

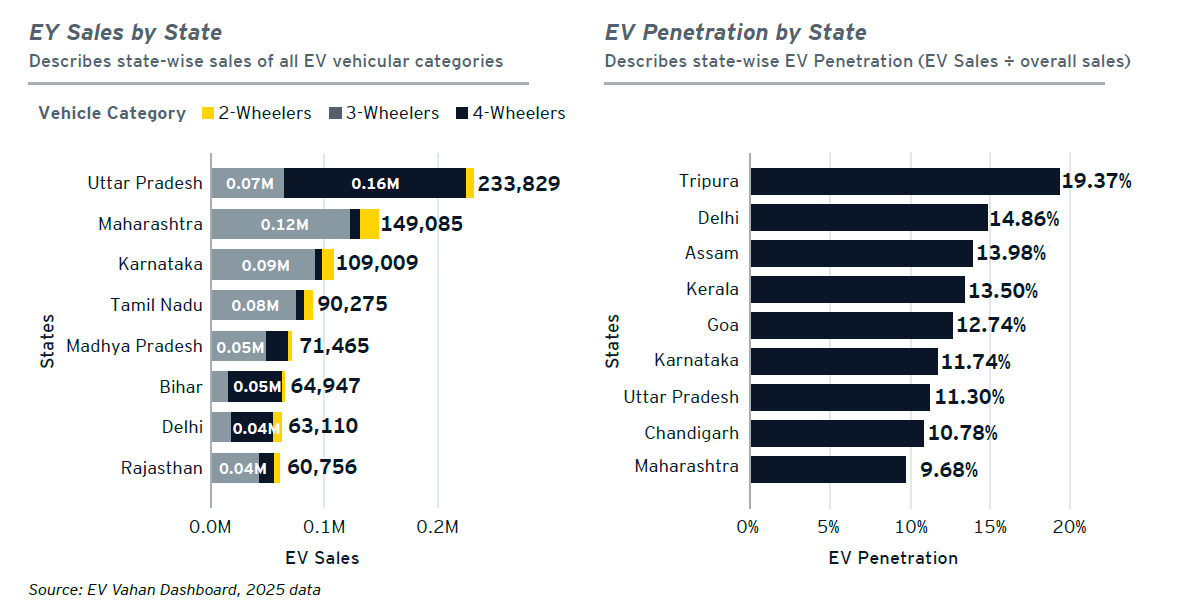

EV adoption in India has accelerated across all vehicle segments, with EV sales expected to reach 12.8 million units annually by FY30 according to the India Energy Storage Alliance (IESA), achieving an overall vehicle penetration rate of 28%. This growth trajectory reflects the convergence of government policy support, technological advancement, and changing consumer preferences driven by economic and environmental considerations.

Two-wheelers dominate India’s EV landscape, holding approximately 90% market share by vehicle type. The sales of electric two-wheelers have increased approximately five times from FY21 to FY24. Large private fleet operators control most of the market share, representing the emergence of organized fleet operations and importance of operational scale in achieving cost competitiveness.

Three-wheeler EV sales have grown at 45% CAGR (FY20-FY24), making India the largest three-wheeler electric market globally, surpassing China in 2023. The lower total cost of ownership and supportive incentives under the FAME II scheme have been instrumental in achieving this market leadership position.

Electric four-wheelers represent the segment with the highest growth potential despite currently having the lowest penetration compared to two-wheelers and three-wheelers. Sales have grown approximately 150% over the last five years, driven by purchase incentives, supply-side support through PLI schemes, tax advantages, and comprehensive awareness campaigns.

Electric four-wheelers represent the segment with the highest growth potential despite currently having the lowest penetration compared to two-wheelers and three-wheelers. Sales have grown approximately 150% over the last five years, driven by purchase incentives, supply-side support through PLI schemes, tax advantages, and comprehensive awareness campaigns.

Policy framework and government support

The central and state governments’ comprehensive policy framework and support has been crucial in accelerating EV adoption, including subsidies, GST reduction and exemptions from permit requirements. State governments have responded enthusiastically to central government initiatives, with states like Uttar Pradesh and Tamil Nadu offering 100% waivers on registration fees for strong hybrid and plug-in hybrid EVs. The increased demand for EVs provides manufacturers opportunities to scale production volumes.

The FAME II scheme has been particularly effective in supporting both demand-side adoption and supply-side development. Government investment of US$125.6 million under FAME II has spurred increases in charging infrastructure while providing purchase incentives.

The PM e-drive scheme allocates INR 2,000 crore to support deployment of 72,300 public charging stations, with 48,400 stations specifically designated for two-wheelers and three-wheelers. The Government launched PM e-Bus Sewa scheme in August 2023 to boost public transport in cities. With a budget of INR 20,000 crore (provided by the central government) for deploying 10,000 electric buses under the Public-Private Partnership (PPP) model, the scheme focuses on making urban travel cleaner and more efficient. These targeted approaches recognize the different charging requirements and usage patterns across vehicle segments.

Manufacturing investments and industrial development

The EV manufacturing sector attracts domestic and international investment, reflecting both market opportunities and government incentives designed to build India’s position as a global EV manufacturing hub. A Swedish company planned a US$1 million investment through its Indian subsidiary to establish a dedicated manufacturing facility in Pune in June 2024. A leading Indian electric two-wheeler manufacturer has committed over INR 2,000 crore to establish a manufacturing unit in Maharashtra. This facility will produce electric two-wheelers and battery packs, expanding the company’s manufacturing footprint beyond its existing facilities in Hosur, Tamil Nadu.

Battery-as-a-Service: Revolutionizing EV economics

Battery-as-a-Service (BaaS) models have emerged as a critical innovation in addressing the high upfront costs associated with electric vehicle adoption, particularly in commercial applications like buses and fleet operations. Since batteries account for 40% to 50% of an electric vehicle’s cost, BaaS models that allow operators to lease rather than purchase batteries significantly reduce initial capital expenditure requirements.

Battery recycling and circular economy

Battery recycling and circular economy

Battery waste management must represent a comprehensive framework for creating a circular economy around battery materials. The Battery Waste Management Rules 2022 mandate that 90% of discarded battery materials must be recycled and recovered by 2026, establishing clear targets for resource recovery. Furthermore, these rules require that 20% of recycled materials be used for manufacturing new batteries by 2030, creating demand for recycled content and incentivizing the development of sophisticated recycling technologies and processes. The demand from end-of-life batteries is estimated to reach 128 GWh by 203037, with 46% (59 GWh) originating from EVs alone—implying a required 60-fold increase in capacity.

Charging infrastructure: Enabling mass EV adoption

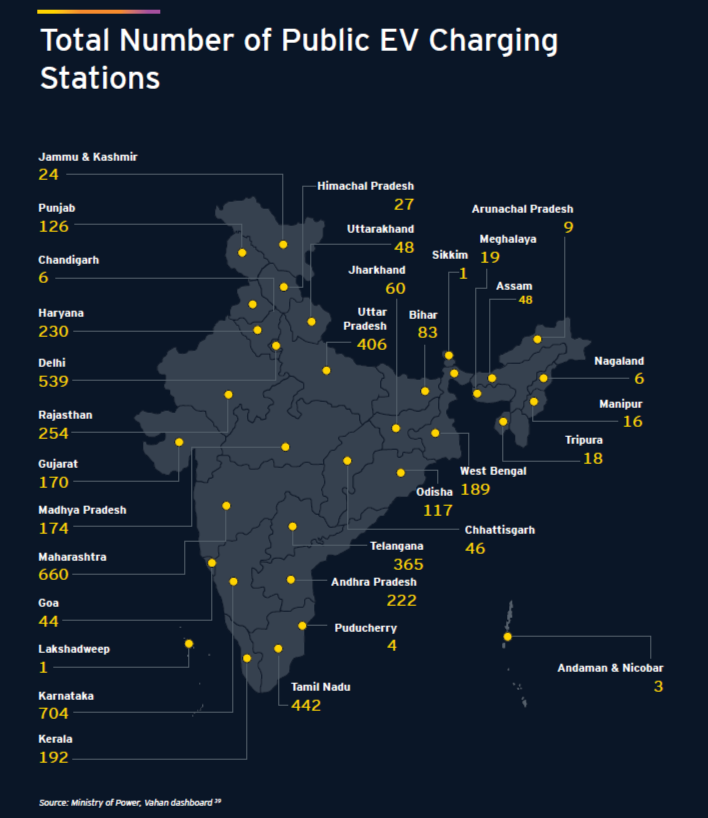

Enabling mass EV adoption. India’s EV charging infrastructure has experienced remarkable expansion, with the number of public charging stations increasing nearly ninefold from 1,800 in February 2022 to more than 26,300 as of early FY 2025. This rapid deployment reflects both government policy support and private sector investment in anticipation of growing EV adoption rates

The Charging Point Operators (CPOs) in India have developed ambitious expansion plans targeting over 100,000 EV charging stations by FY27. The operators have formed strategic partnerships with B2B fleet players to ensure utilization rates while collaborating with real estate players to access key locations for charging infrastructure deployment.

Innovations

Regional investment clusters and innovation hubs

Bengaluru has emerged as India’s premier hub for e-mobility startups and EV innovation, hosting several of the country’s most successful electric vehicle companies. The city’s established technology ecosystem, skilled workforce, and venture capital presence create an ideal environment for EV innovation and scaling.

Delhi-NCR is a major center for renewable energy generation projects and corporate headquarters for large-scale renewable energy companies. This concentration reflects the region’s proximity to policy-making institutions and established industrial infrastructure.

Mumbai’s role as India’s financial capital makes it a natural center for clean energy financing and investments. The city hosts several major corporations that have operational and financial commitments to the sector. Major global financial institutions channel capital through their India teams based in Mumbai. These institutions provide the large-scale funding necessary for renewable energy and green hydrogen project development while bringing international expertise and standards to Indian operations.

Production-Linked Incentives (PLI) and manufacturing development

The PLI Scheme represents a strategic approach to building domestic manufacturing capabilities across critical clean energy technologies. The PLI framework spans 14 major sectors, with a total incentive outlay of around INR 1.97 lakh crore. The government has launched targeted PLI programs for battery manufacturing, electrolyzer production, and green hydrogen production, creating comprehensive support for the entire clean energy value chain. To date, the scheme has attracted INR 67,690 crore in committed investments, and generated over 28,800 jobs. The Advanced Chemistry Cell PLI scheme, worth INR 18,100 crore, specifically targets battery manufacturing to build India’s capabilities in this critical technology area.

Innovation in business models and financing

One platform exemplifies innovative approaches to renewable energy financing and market development. By supplying round-the-clock renewable power to a resources group and other commercial and industrial consumers, it demonstrates the integration of renewable energy generation with assured industrial demand. The integration of renewable energy supply with industrial demand represents a critical innovation for scaling green hydrogen production, as it provides the long-term power purchase agreements necessary for project financing while ensuring that renewable capacity additions are matched with corresponding demand growth.

Transportation applications and hydrogen mobility

India has initiated five pilot projects under the National Green Hydrogen Mission specifically focused on transportation applications, deploying 37 hydrogen-powered vehicles across diverse operational environments, providing comprehensive real-world testing of different hydrogen mobility technologies. The government has allocated INR 208 crore (US$25.06 million) for these pilot projects, which include both vehicles and supporting infrastructure development. Nine hydrogen refueling stations are being established as part of these pilots, with operations expected to commence within 18-24 months.

Technology advancement and R&D

Energy storage technology advancement focuses on improving battery performance, reducing costs, and enhancing grid integration capabilities. The growth of smart grid integration enables dynamic response to grid conditions and optimized energy management across distributed generation resources.

Advanced battery management systems coordinate with grid operators to provide real-time balancing services while maximizing economic returns for storage operators. These systems enable storage assets to participate in multiple revenue streams including energy arbitrage, frequency regulation, and capacity markets.

The development of hybrid renewable energy systems combining solar, wind, and storage components enables round-theclock renewable power delivery while providing grid services that enhance overall system reliability.

Recommendations

India stands at the cusp of a transformative clean energy and electric mobility revolution. The country now needs to leverage its rapidly growing renewable energy capacity while increasing strategic investments in green hydrogen and expanding electric mobility market by continuing and strengthening coordinated efforts across innovation hubs, regional industrial clusters, and manufacturing ecosystems. Some of the steps that India should take to emerge as a leader in clean and sustainable energy are:

- Scaling renewable capacity aggressively to meet the target of 500 GW of non-fossil fuel electricity by 2030, a goal India is advancing towards ahead of schedule, having crossed 50% non-fossil capacity already.

- Expanding green hydrogen production under the National Green Hydrogen Mission, targeting 5 million tons per year by 2030 with planned investments exceeding INR8 lakh crore and creation of over 600,000 jobs.

- Accelerating electric mobility adoption supported by government schemes like FAME, aiming for 30% EV market share by 2030 and substantial employment generation.

- Strengthening the domestic manufacturing ecosystem, especially for battery technologies, electrolysers, and solar/wind components, supported by investment-friendly policies and 100% FDI under the automatic route.

- Promoting circular economy practices and sustainable infrastructure development to enhance resource efficiency and lifecycle emissions reduction.

- Sustaining policy frameworks that stimulate private sector investment, innovation, and long-term demand through renewable purchase obligations, tendering for clean power, and transmission charge waivers.

- Facilitating energy transition in hard-to-electrify sectors through green hydrogen and other clean fuels.

- Building India as a global exemplar for inclusive economic growth driven by clean, secure, and affordable energy.

This holistic and integrated approach, backed by strong policy commitments and growing markets, is essential to accelerate India’s energy transition, meet its net-zero by 2070 target, and position the country as a global leader and blueprint in sustainable energy and electric mobility.

Access the full report here.