Hydrogen Generation

Market Summary

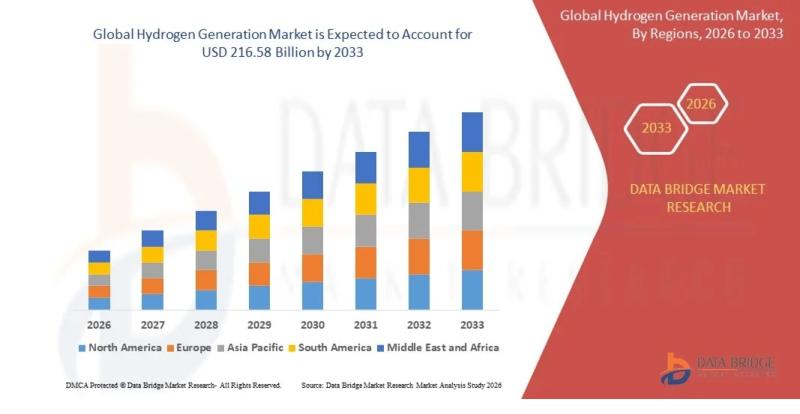

As per Data Bridge Market Research analysis, the Hydrogen Generation Market was estimated at USD 153.46 billion in 2025. The market is expected to grow from USD 160.21 billion in 2026 to USD 216.58 billion in 2033, at a CAGR of 4.40% during the forecast period with driven by the rising demand for clean energy solutions, industrial decarbonization, and expanding applications across refining, ammonia production, and transportation sectors.

Market Size & Forecast

2025 Market Size: USD 153.46 Billion

2026 Projected Market Size: USD 160.21 Billion

2033 Projected Market Size: USD 216.58 Billion

CAGR (2026-2033): 4.40%

Largest Region: North America

Fastest Growing Region: Asia Pacific

Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs): https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-hydrogen-generation-market

Key Market Report Takeaways

North America holds the largest market share (~35-38%) due to established hydrogen infrastructure and strong industrial demand

Asia Pacific is the fastest-growing region, driven by rapid industrialization and government-backed hydrogen initiatives

Steam methane reforming (SMR) dominates as the leading hydrogen production process due to cost efficiency

Grey hydrogen remains the largest segment, though blue and green hydrogen are gaining traction

Refining industry accounts for the highest end-use share due to extensive hydrogen consumption in hydrocracking and desulfurization

Market Trends & Highlights

North America leads the global market due to mature refining infrastructure, high hydrogen consumption, and strong investment in carbon capture technologies

Asia Pacific is the fastest-growing region, supported by large-scale hydrogen projects, policy incentives, and growing energy demand in China, India, and Japan

Industrial applications, particularly petroleum refining and ammonia production, remain the dominant segments due to consistent demand

Key growth drivers include decarbonization mandates, rising energy demand, and increasing investments in hydrogen infrastructure

Emerging technologies such as electrolysis-based green hydrogen and carbon capture integration are reshaping production methods

Regulatory frameworks, public-private partnerships, and national hydrogen strategies are accelerating global market expansion

Looking For Full Report? Get it Here: https://www.databridgemarketresearch.com/reports/global-hydrogen-generation-market

Market Dynamics

Market Drivers

Rising Demand for Clean Energy Transition

Global efforts to reduce carbon emissions are driving demand for hydrogen as a clean energy carrier. Governments across Europe and Asia Pacific are promoting hydrogen adoption through net-zero targets and decarbonization policies. Hydrogen is increasingly used in power generation, transportation, and industrial processes. This transition is significantly boosting investment in green and blue hydrogen technologies.

Expansion of Refining and Chemical Industries

Hydrogen is widely used in refining processes such as hydrocracking and desulfurization. Growing demand for low-sulfur fuels globally is increasing hydrogen consumption. Additionally, ammonia and methanol production industries rely heavily on hydrogen. Industrial expansion in emerging economies is further supporting sustained demand growth.

Technological Advancements in Hydrogen Production

Innovations in electrolysis and carbon capture technologies are improving efficiency and reducing environmental impact. Proton exchange membrane (PEM) and alkaline electrolysis systems are gaining traction. Integration of renewable energy sources into hydrogen production is accelerating the shift toward green hydrogen. These advancements are enhancing scalability and commercial viability.

Government Policies and Incentives

Governments worldwide are introducing subsidies, tax incentives, and funding programs to promote hydrogen adoption. National hydrogen strategies in regions such as Europe and Asia Pacific are encouraging infrastructure development. Regulatory frameworks supporting clean energy are facilitating investments in hydrogen projects. These initiatives are strengthening market growth prospects.

Growing Investments and Strategic Partnerships

Major energy companies and governments are investing heavily in hydrogen infrastructure and production facilities. Strategic collaborations between private and public sectors are accelerating project deployment. Increasing funding for research and development is fostering innovation. These investments are driving long-term market expansion globally.

Market Restraints

High Production and Infrastructure Costs

Hydrogen production, particularly green hydrogen, involves high capital expenditure due to expensive electrolysis equipment and renewable energy integration. Infrastructure for storage and transportation also requires significant investment. These high costs limit adoption, especially in developing regions. Cost competitiveness with conventional fuels remains a challenge.

Dependence on Fossil Fuel-Based Hydrogen

A significant portion of hydrogen production still relies on fossil fuels, particularly natural gas. Grey hydrogen production contributes to carbon emissions, contradicting sustainability goals. Transitioning to cleaner alternatives requires substantial investment. This dependency slows the pace of market transformation.

Storage and Transportation Challenges

Hydrogen has low energy density, making storage and transportation complex and costly. Specialized infrastructure such as high-pressure tanks and pipelines is required. Safety concerns associated with hydrogen handling also pose challenges. These factors limit widespread adoption across regions.

Regulatory and Standardization Issues

Lack of uniform global standards for hydrogen production, storage, and distribution creates regulatory complexities. Different regions have varying policies and safety guidelines. Compliance requirements can delay project implementation. This fragmentation affects market scalability and cross-border trade.

Limited Renewable Energy Integration

Green hydrogen production depends on renewable energy availability, which is inconsistent in many regions. Intermittency of solar and wind power affects production efficiency. Limited renewable infrastructure in developing economies further restricts growth. This dependency impacts long-term sustainability goals.

Market Opportunities

Growth of Green Hydrogen Economy

The transition toward green hydrogen presents significant growth opportunities. Increasing investments in renewable energy integration are enabling sustainable hydrogen production. Governments are prioritizing green hydrogen projects to achieve climate targets. This shift is expected to generate substantial revenue opportunities over the forecast period.

Expansion in Emerging Markets

Developing regions such as Asia Pacific, Latin America, and the Middle East offer untapped potential. Rapid industrialization and rising energy demand are driving hydrogen adoption. Government initiatives in countries like India and China are supporting infrastructure development. These markets present strong growth prospects for industry players.

Hydrogen in Transportation Sector

The adoption of hydrogen fuel cells in transportation is creating new growth avenues. Applications include fuel cell vehicles, buses, and heavy-duty trucks. Increasing focus on zero-emission mobility is driving demand. Investments in hydrogen refueling infrastructure are further supporting this segment.

Strategic Collaborations and Investments

Partnerships between energy companies, technology providers, and governments are accelerating market growth. Joint ventures are enabling large-scale hydrogen production projects. Increasing venture capital investments in hydrogen startups are fostering innovation. These collaborations are expanding market reach and capabilities.

Integration with Renewable Energy Systems

Hydrogen is emerging as a key solution for energy storage and grid balancing. Integration with solar and wind energy systems enhances energy efficiency. Power-to-gas technologies are gaining popularity in developed regions. This integration supports long-term sustainability and energy transition goals.

Market Challenges

Infrastructure Development Limitations

The lack of adequate hydrogen infrastructure, including pipelines and refueling stations, is a major challenge. Developing such infrastructure requires significant capital and long timelines. Many regions, especially developing economies, face limitations in deployment. This restricts market penetration and scalability.

Technological Maturity and Scalability Issues

While hydrogen technologies are evolving, large-scale commercialization remains limited. Electrolysis systems and carbon capture technologies require further optimization. Scalability challenges impact cost efficiency and production capacity. These limitations hinder widespread adoption.

Supply Chain Constraints

Hydrogen production relies on critical raw materials and components such as electrolyzers and catalysts. Supply chain disruptions can affect production timelines and costs. Dependence on specific suppliers increases vulnerability. These constraints impact market stability and growth.

Economic and Price Volatility

Fluctuations in natural gas prices directly affect hydrogen production costs, especially for grey and blue hydrogen. Economic uncertainties can impact investment decisions. Price volatility creates challenges for long-term project planning. This affects market profitability and expansion.

Competition from Alternative Energy Sources

Hydrogen faces competition from other renewable energy solutions such as battery storage and electrification. In some applications, alternatives may offer lower costs or higher efficiency. This competition impacts adoption rates across industries. Market players must differentiate through innovation and cost optimization.

Get Detailed Insights Before You Buy – Request Complete Market Intelligence Now.

https://www.databridgemarketresearch.com/checkout/buy/global-hydrogen-generation-market/compare-licence

Market Segmentation & Analysis

By Type (Grey, Blue, Green Hydrogen)

Grey hydrogen dominates the market with the highest share due to its cost-effectiveness and established production methods. Blue hydrogen is gaining traction due to carbon capture integration, particularly in North America and Europe. Green hydrogen is the fastest-growing segment, supported by renewable energy adoption and government incentives. Increasing investments in electrolysis technologies are accelerating growth. The green hydrogen segment is expected to register the highest CAGR during the forecast period.

By Production Process (Steam Methane Reforming, Electrolysis, Coal Gasification)

Steam methane reforming (SMR) holds the largest market share due to its widespread industrial use and lower production costs. Electrolysis is the fastest-growing segment, driven by the shift toward sustainable energy solutions. Coal gasification remains relevant in regions with abundant coal reserves. Technological advancements are improving efficiency across processes. Electrolysis is expected to witness strong growth due to increasing green hydrogen demand.

By Application (Refining, Ammonia Production, Methanol Production, Transportation, Power Generation)

Refining is the dominant application segment, accounting for the largest share due to high hydrogen consumption in fuel processing. Ammonia production is another significant segment driven by fertilizer demand. Transportation is the fastest-growing application due to increasing adoption of fuel cell vehicles. Power generation is emerging as a key segment with hydrogen-based energy storage solutions.

By End-User (Oil & Gas, Chemicals, Energy, Transportation, Others)

The oil & gas sector leads the market due to extensive hydrogen use in refining operations. The chemical industry also holds a substantial share due to ammonia and methanol production. The transportation sector is the fastest-growing end-user segment, driven by clean mobility initiatives. The energy sector is expanding with increasing hydrogen integration in power systems.

Analytical Insights

Largest Segment: Grey hydrogen due to cost efficiency and established infrastructure

Fastest-Growing Segment: Green hydrogen due to sustainability goals and policy support

Dominance driven by industrial demand and established production technologies

Growth driven by clean energy transition and technological advancements

Regional Analysis

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America dominates the hydrogen generation market, accounting for approximately 35-38% of global revenue. The region benefits from advanced infrastructure, strong presence of key market players, and high hydrogen demand in refining industries. The United States is the primary contributor due to large-scale industrial applications and investments in carbon capture technologies. Government policies supporting clean energy transition further strengthen market growth.

Europe

Europe represents a mature market with steady growth driven by strong regulatory frameworks and sustainability initiatives. Countries such as Germany, the U.K., and France are investing heavily in hydrogen technologies. The European Union’s hydrogen strategy is accelerating adoption across industries. Increased R&D investments and focus on green hydrogen are supporting long-term growth.

Asia Pacific

Asia Pacific is the fastest-growing region due to rapid industrialization and increasing energy demand. China, India, and Japan are leading contributors with significant investments in hydrogen infrastructure. Government support and favorable policies are driving adoption. Expanding manufacturing and chemical industries further boost demand in the region.

Latin America

Latin America is an emerging market with gradual growth supported by infrastructure development and renewable energy projects. Brazil and Mexico are key contributors with increasing investments in clean energy. However, economic constraints and limited technological adoption pose challenges. The region shows potential for future growth with supportive policies.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth driven by investments in energy diversification. Governments are focusing on hydrogen as part of long-term sustainability strategies. Private sector participation is increasing, particularly in the Middle East. However, infrastructure limitations and regulatory gaps slow market expansion.

Key Insights:

Largest Region: North America

Fastest Growing Region: Asia Pacific

Mature Markets: North America, Europe

High-Growth Markets: Asia Pacific

Emerging Markets: Latin America, Middle East & Africa

Competitive Landscape

Market Structure Overview

The hydrogen generation market is moderately consolidated with the presence of global energy giants and regional players. Competition is driven by technological innovation, production efficiency, and strategic partnerships. Leading companies focus on expanding their hydrogen portfolios and investing in sustainable solutions. Competitive analysis helps understand market positioning and strategic direction of key players.

Key Industry Players

Leading players operate across integrated value chains, focusing on production technologies, infrastructure, and global expansion. Companies are strengthening their market presence through innovation and strategic collaborations.

Air Liquide

Linde plc

Air Products and Chemicals, Inc.

Shell plc

BP plc

Plug Power Inc.

Siemens Energy

Nel ASA

Toshiba Energy Systems & Solutions

Cummins Inc.

Competitive Strategies

Companies are focusing on product innovation and development of green hydrogen technologies. Strategic partnerships and joint ventures are accelerating large-scale hydrogen projects. Mergers and acquisitions are being used to strengthen market presence. Geographic expansion into emerging markets is a key growth strategy. These initiatives enhance competitive advantage and customer value proposition.

Emerging Players & Market Dynamics

Startups and niche players are entering the market with innovative and cost-effective solutions. Increasing funding and investments are fostering competition. Emerging companies are focusing on green hydrogen and advanced electrolysis technologies. Digital transformation and technological advancements are reshaping the competitive landscape.

Latest Developments

January 2025 – Air Liquide: Announced expansion of green hydrogen production capacity in North America,

strengthening its position in sustainable hydrogen solutions and supporting decarbonization efforts.

October 2024 – Linde plc: Launched a large-scale hydrogen production facility integrated with carbon capture

technology, enhancing efficiency and reducing emissions.

June 2024 – Shell plc: Partnered with renewable energy providers to develop green hydrogen projects in Europe, accelerating energy transition initiatives.

March 2024 – Plug Power Inc.: Secured funding for expansion of hydrogen fuel cell infrastructure in the U.S., boosting adoption in transportation and logistics sectors.

November 2023 – Siemens Energy: Introduced advanced electrolysis technology aimed at improving hydrogen production efficiency and scalability.

September 2023 – BP plc: Invested in hydrogen hubs in Asia Pacific, supporting regional growth and clean energy adoption.

July 2023 – Nel ASA: Expanded manufacturing capacity for electrolyzers, addressing growing demand for green hydrogen production systems.

Check out more related studies published by Data Bridge Market Research:

https://www.databridgemarketresearch.com/reports/global-silicon-metal-market

https://www.databridgemarketresearch.com/reports/global-d-limonene-market

https://www.databridgemarketresearch.com/reports/global-helium-3-market

https://www.databridgemarketresearch.com/reports/global-biofuels-market

https://www.databridgemarketresearch.com/reports/global-corrosion-protection-coatings-market

https://www.databridgemarketresearch.com/reports/global-mining-tailings-management-market

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com

Data Bridge Market Research is dedicated to deliver market intelligence with highest quality and accuracy. Through meticulous analysis and research, we strive to provide our clients with reliable and precise insights into various industries and markets. Over 500 full-time analysts at Data Bridge Market Research follow a wide array of models that allow proactive collaboration with clients, categorize new sources of incremental revenues, deliver revenue planning, and first-mover advantage about innovations and disruptions through early market research.

This release was published on openPR.