Green Hydrogen Market

The global green hydrogen market reached US$ 7.98 billion in 2024, rising to US$ 10.95 billion in 2025 and is expected to reach US$ 147.61 billion by 2033, growing at a strong CAGR of 38.6% from 2026 to 2033. as industries and governments worldwide accelerate investments in clean energy solutions to decarbonize hard-to-abate sectors and support climate goals.

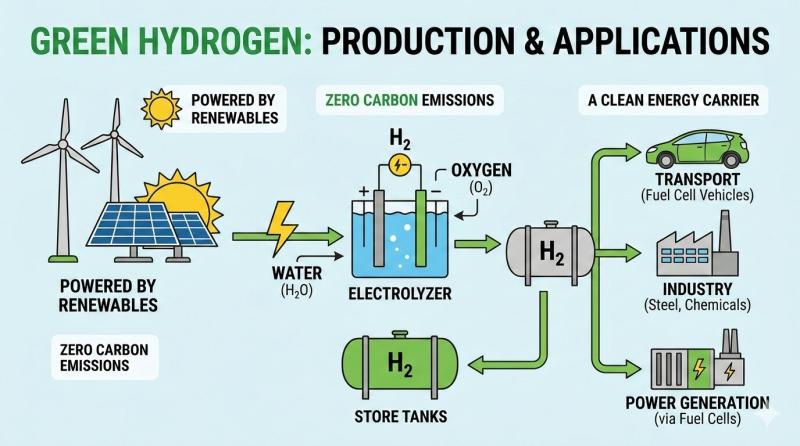

Growth is supported by increasing demand across key applications such as transportation (including fuel cell vehicles), power generation, industrial heat and feedstock, and energy storage, driven by favorable regulatory frameworks, ambitious net-zero targets, and declining costs of renewable energy and electrolyzer technologies. Expansion of large-scale electrolyzer manufacturing, supportive policy incentives (such as tax credits, carbon pricing, and green hydrogen mandates), and strategic partnerships between public and private stakeholders further accelerate market adoption. Additionally, growing focus on sustainable industrial processes, hydrogen export opportunities, and integration of green hydrogen into broader hydrogen value chains continue to propel broad utilization of green hydrogen solutions worldwide.

Download your exclusive sample report today (corporate email gets priority access):

https://www.datamintelligence.com/download-sample/green-hydrogen-market?sindhuri

Green Hydrogen Market: Competitive Intelligence

Air Liquide S.A., Linde plc, Siemens Energy AG, Nel ASA, Plug Power Inc., ITM Power plc, Ballard Power Systems Inc., Cummins Inc. (Hydrogenics), Engie SA, and others.

The Green Hydrogen Market is strongly driven by leading energy, industrial gas, equipment manufacturing, and power technology companies such as Air Liquide S.A., Linde plc, Siemens Energy AG, Nel ASA, and Plug Power Inc., who develop and supply green hydrogen production technologies including alkaline electrolyzers, proton exchange membrane (PEM) electrolyzers, integrated hydrogen generation systems, and renewable-energy-linked hydrogen solutions designed to produce hydrogen using renewable electricity with minimal carbon emissions. These offerings support decarbonization efforts across power generation, transportation (fuel-cell vehicles), industrial processes (steel, chemicals), and energy storage applications.

Increasing global commitments to net-zero emissions, aggressive governmental renewable energy targets and incentives, declining renewable electricity generation costs, and rising industrial demand for low-carbon fuels are key factors fueling green hydrogen market growth. Additionally, strategic alliances between energy utilities, original equipment manufacturers (OEMs), and technology developers are accelerating development of large-scale electrolyzer projects, hydrogen hubs, and integrated renewable hydrogen supply chains in Europe, Asia-Pacific, and North America.

These companies’ complementary strengths comprehensive industrial gas and hydrogen ecosystem solutions from Air Liquide and Linde; electrification and power-system integration expertise from Siemens Energy; electrolyzer technology leadership and deployment scale from Nel and ITM Power; fuel-cell and hydrogen-infrastructure innovations from Plug Power and Ballard Power Systems; and diversified renewable energy and project development experience from Engie and Cummins (Hydrogenics) enhance competitive positioning across the green hydrogen value chain. Strategic focus areas include development of high-efficiency, low-cost electrolyzers, expansion of gigawatt-scale green hydrogen production facilities, integration with renewable power sources (such as solar and wind), establishment of hydrogen refueling and distribution infrastructure, and partnerships with governments, utilities, and industrial users to accelerate adoption of green hydrogen solutions globally.

Get Customization in the report as per your requirements:

https://www.datamintelligence.com/customize/green-hydrogen-market?sindhuri

Recent Key Developments – United States & North America

✅ June 2025: Plug Power expanded its green hydrogen production facilities in the U.S., increasing electrolyzer capacity to support mobility, industrial decarbonization, and energy storage applications.

✅ May 2025: Air Products and Chemicals, Inc. advanced large-scale green hydrogen projects across North America, integrating renewable-powered electrolysis to supply refineries, ammonia producers, and heavy transport sectors.

✅ 2025: The U.S. government accelerated hydrogen hub development under the Infrastructure Investment and Jobs Act, driving investments in regional clean hydrogen clusters and strengthening domestic production ecosystems.

Recent Key Developments – Japan & Asia-Pacific

✅ July 2025: Mitsubishi Heavy Industries expanded green hydrogen demonstration projects in Japan, focusing on integrating electrolyzers with offshore wind and solar energy systems.

✅ Early 2026: Adani New Industries Limited launched large-scale green hydrogen and ammonia production initiatives in India, targeting export markets and domestic industrial decarbonization.

✅ 2025: Countries including Australia, South Korea, and China increased investments in hydrogen infrastructure, storage solutions, and export-oriented projects to establish Asia-Pacific as a key green hydrogen production hub.

Recent Key Developments – Product & Technology Innovation

✅ 2025: Advanced Electrolyzer Technologies: Manufacturers introduced high-efficiency PEM and solid oxide electrolyzers capable of improving hydrogen output while reducing energy consumption and capital costs.

✅ Hydrogen Storage & Transport Innovations: Development of liquid hydrogen carriers, ammonia-based transport systems, and advanced compression technologies enhanced supply chain feasibility.

✅ Renewable Integration & Digital Optimization: Integration of AI-driven energy management systems optimized renewable power usage for electrolysis, improving operational efficiency and reducing production costs.

1. M&A / Strategic Activity

Strategic industry consolidation and partnerships shaping the green hydrogen ecosystem:

Power2X acquires HyCC to strengthen its clean molecule portfolio Power2X completed its acquisition of European hydrogen producer HyCC, combining development pipelines in the Netherlands and Germany and consolidating project delivery capacity for large-scale green hydrogen and related clean molecules. This transaction enhances project scale and investment leverage in the decarbonization value chain.

Large strategic partnerships announced at ACWA Innovation Days 2026 Saudi clean energy leader ACWA Power unveiled 27 strategic partnerships across governments, research institutions, and global energy players focused on scaling hydrogen solutions, underlining the Kingdom’s role as a strategic green hydrogen hub and testbed for integrated water-energy solutions.

Oil & gas firms negotiating low-emission derivative projects Industrial gases major Air Products is in advanced negotiations with Yara International on low-emission ammonia and hydrogen initiatives, potentially expanding hydrogen’s industrial footprint.

✅ 2. New Projects & Deployments

Recent large-scale green hydrogen projects and commercial initiatives:

NeuEN Green wins 10,000 MTPA green hydrogen project at Assam’s Numaligarh Refinery NeuEN Green Energy secured a landmark contract to build and operate a 10,000 metric-tons-per-annum green hydrogen facility to supply renewable hydrogen to Numaligarh Refinery on a BOO basis, integrating renewable energy and biomass feedstock sourcing.

Moeve (formerly Cepsa) and Masdar launch €1.2 billion Andalusian project Spanish energy company Moeve, backed by Masdar and investors, announced a 300 MW green hydrogen plant in Andalusia one of the largest in southern Europe supported by €300 million in EU subsidies, showing continued long-term infrastructure commitment.

Port of Newcastle FEED for hydrogen export hub – In Australia, the Port of Newcastle completed Front-End Engineering Design (FEED) for a 1.5 GW renewable green hydrogen and derivative export hub, aiming for operations by 2030 and positioning the region for large-scale clean export markets.

Germany continues major green H2 infrastructure investment Germany approved funding and rollout of its National Hydrogen Strategy, including large electrolyzer projects (e.g., 500 MW with offshore wind integration) and a hydrogen backbone network to connect production and demand.

✅ 3. R&D & Technological Advancements

Electrolyzer Innovations & Next-Gen Systems

Solid Oxide Electrolyzer (SOEC) systems capable of high-temperature operation and reduced electricity consumption are emerging as the fastest-growing technology segment, particularly for commercial and industrial integration.

AI-Driven Materials Design

Academic research is accelerating the design of proton exchange membranes for electrolyzers using AI-accelerated materials discovery, aiming to reduce dependence on costly fluorinated membranes and lower total system capital costs.

System Cost Optimization Strategies

R&D is exploring multi-market optimization for electrolyzer operation balancing electricity market participation to minimize operational costs or even create arbitrage revenue streams which could improve financial viability in real-world electricity markets.

End-Use Integration R&D

Green hydrogen applications in heavy industry (e.g., direct reduced iron for low-carbon steel), refining decarbonization, and chemical feedstocks are being piloted with integrated electrolyzer systems, as green hydrogen becomes central to hard-to-abate sectors.

Buy Now & Unlock 360° Market Intelligence:

https://www.datamintelligence.com/buy-now-page?report=green-hydrogen-market?sindhuri

Segments Covered in the Green Hydrogen Market:

By Technology

The market is segmented into alkaline electrolyzer (AEL) (45%), proton exchange membrane (PEM) (30%), solid oxide electrolyzer (SOEC) (10%), anion exchange membrane (AEM) (8%), and biomass pyrolysis (7%).Alkaline electrolyzers dominate due to their commercial maturity, lower capital costs, and large-scale industrial deployment. PEM technology is rapidly growing because of higher efficiency, compact design, and suitability for variable renewable energy integration. SOEC is gaining traction for high-temperature industrial applications with improved efficiency potential. AEM and biomass pyrolysis are emerging technologies with growing R&D investments. Increasing decarbonization targets and government incentives are accelerating technological advancements across segments.

By Renewable Source

Renewable sources include wind (35%), solar (30%), hydropower (15%), hybrid systems (10%), biomass/bioenergy (5%), and nuclear-powered electrolysis (5%).Wind energy dominates due to large-scale offshore and onshore wind projects integrated with electrolyzers. Solar-based hydrogen production is expanding rapidly, particularly in regions with high solar irradiation. Hydropower remains stable due to consistent power supply for electrolysis. Hybrid systems combining solar and wind are gaining popularity for ensuring continuous hydrogen production. Nuclear-powered electrolysis is emerging in advanced economies focusing on low-carbon baseload energy integration.

By Application

Applications comprise industrial feedstock (30%), power & grid (20%), transport/mobility (20%), energy storage (15%), heating (10%), and others (5%).Industrial feedstock dominates due to strong demand from ammonia, methanol, and refining industries seeking to reduce carbon emissions. Power & grid applications are expanding with hydrogen-based power generation and grid balancing solutions. Transport and mobility are growing rapidly with fuel cell vehicles, buses, trucks, and maritime adoption. Energy storage applications support renewable integration and long-duration storage solutions. Heating applications are emerging in residential and industrial decarbonization strategies.

Regional Analysis

Europe – 35% Share

Europe leads the market supported by ambitious hydrogen strategies, carbon neutrality targets, and strong government subsidies. Countries such as Germany, France, Spain, and the Netherlands are investing heavily in large-scale green hydrogen projects and cross-border hydrogen infrastructure.

Asia-Pacific – 30% Share

Asia-Pacific holds a significant share driven by hydrogen roadmaps in China, Japan, South Korea, and Australia. Rapid industrialization, renewable energy expansion, and export-oriented hydrogen production projects accelerate regional growth.

North America – 20% Share

North America is witnessing strong growth with supportive policies, tax incentives, and investments in hydrogen hubs, particularly in the United States and Canada. Industrial decarbonization and clean mobility initiatives fuel adoption.

Request for 2 Days FREE Trial Access:

https://www.datamintelligence.com/reports-subscription?sindhuri

✅ Competitive Landscape

✅ Technology Roadmap Analysis

✅ Sustainability Impact Analysis

✅ KOL / Stakeholder Insights

✅ Consumer Behavior & Demand Analysis

✅ Import-Export Data Monitoring

✅ Live Market & Pricing Trends

Contact Us –

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: Sai.k@datamintelligence.com

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

About Us –

DataM Intelligence is a Market Research and Consulting firm that provides end-to-end business solutions to organizations from Research to Consulting. We, at DataM Intelligence, leverage our top trademark trends, insights and developments to emancipate swift and astute solutions to clients like you. We encompass a multitude of syndicate reports and customized reports with a robust methodology.

Our research database features countless statistics and in-depth analyses across a wide range of 6300+ reports in 40+ domains creating business solutions for more than 200+ companies across 50+ countries; catering to the key business research needs that influence the growth trajectory of our vast clientele.

This release was published on openPR.