Support CleanTechnica’s work through a Substack subscription or on Stripe.

Or support our Kickstarter campaign!

The October 2025 special report from Germany’s Federal Audit Court, Implementation of the Federal Government’s Hydrogen Strategy, lands with unusual weight because it is not a policy critique or an academic intervention, but a statutory budgetary assessment delivered to Parliament. It evaluates the hydrogen strategy against the legal requirements of the Energy Industry Act, namely security of supply, affordability, environmental sustainability, climate neutrality, and fiscal prudence. Its conclusion is that the hydrogen strategy is not meeting these tests, despite €4.3 billion allocated in 2024, more than €3 billion in 2025, and multi-billion-euro commitments extending through the end of the decade. The report explicitly calls for a reality check and a plan B, warning that continuing on the current trajectory risks climate goals, industrial competitiveness, and federal finances at the same time.

The audit establishes early that the hydrogen economy Germany planned for 2030 does not resemble the one now unfolding. Domestic electrolysis capacity was set at 10 GW by 2030, but less than 0.2 GW was operating by 2025 and fewer than 5 GW are now expected by 2030. On the import side, the mismatch is more severe. Global green hydrogen production with final investment decisions amounts to about 63 TWh for 2030, while Germany alone projected import demand of 47.5 TWh at the low end and up to 91 TWh at the high end. Even under optimistic assumptions, Germany would need to secure three quarters of global supply, a result the audit treats as implausible rather than ambitious. Programs such as H2Global and the Green Hydrogen Fund have not materially changed this picture, with one awarded import lot still lacking a final investment decision and the Green Hydrogen Fund yet to disburse capital.

Demand was meant to solve this supply problem. The hydrogen strategy assumed that industrial users and hydrogen-fired power plants would provide anchor demand that justified early infrastructure build-out. The audit shows that this demand has not materialized. Four subsidized steel projects were expected to account for more than 18 TWh of annual hydrogen demand. One has already stepped away, and the others face uncertain timelines and availability of green hydrogen. Carbon Contracts for Difference were expected to broaden industrial demand, but only a minority of awarded contracts actually involve hydrogen. In the power sector, the planned role of hydrogen has been quietly reduced. Hydrogen-ready power plants were scaled back from 23.8 GW to 7.5 GW by 2040, and even these no longer carry binding requirements to switch from natural gas to hydrogen. Without legal offtake obligations, the audit concludes that a key driver of hydrogen demand is missing.

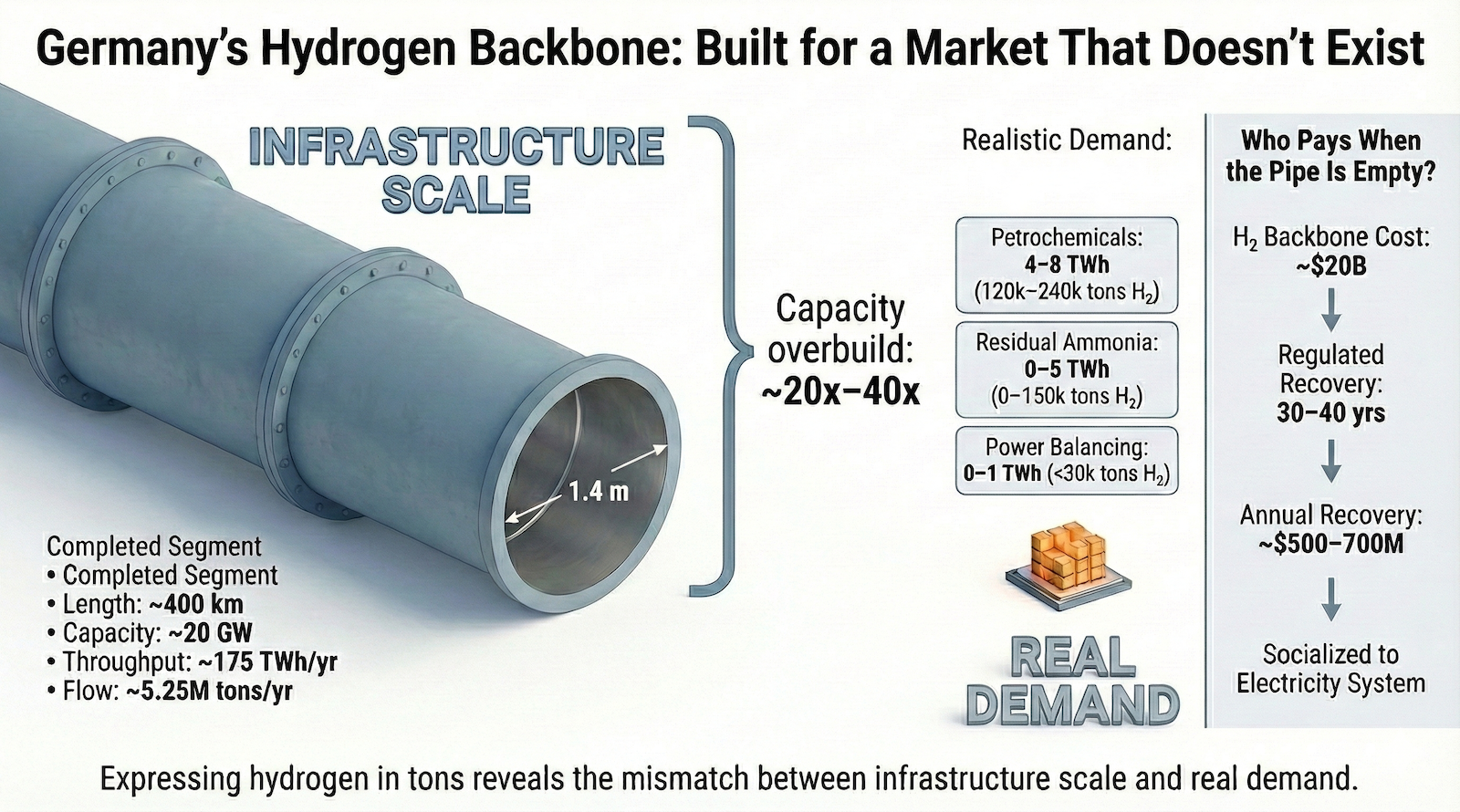

Against this backdrop, Germany approved a hydrogen core network of 9,040 km, designed for 87 GW of withdrawal capacity and 101 GW of feed-in capacity by 2032. More than two thirds of this network is scheduled to be operational by 2030. This decision assumed synchronized ramp-up of supply, demand, and infrastructure. The audit demonstrates that synchronization has failed. Supply will be late, demand is uncertain, and infrastructure is arriving early. Several segments of the backbone are no longer theoretical. Steel is in the ground and sections are pressurized. That technical detail matters because pressurization changes the nature of the asset. It is no longer optional capacity waiting on future decisions, but active infrastructure with operating costs, safety obligations, and fiscal consequences.

The financing structure of the hydrogen backbone turns early operation into direct public exposure. Network charges are capped during the ramp-up phase, with shortfalls covered through an amortization account funded by a state-guaranteed loan from KfW, Germany’s state-owned development bank. That loan facility reaches up to €24 billion. Repayment depends on future network utilization, meaning on hydrogen producers and consumers connecting at scale. If that utilization does not materialize, the financing mechanism fails. In that case, the federal government bears at least 76% of the remaining shortfall, implying public liability exceeding €18 billion if the loan is fully drawn. Interim financing costs alone are estimated between €5 billion and €16.3 billion through 2055, depending on utilization and interest rates.

A pressurized pipeline segment with no contracted suppliers and no committed offtakers worsens these risks rather than holding them constant. It draws on the amortization account immediately, increases interim financing costs, and raises per-unit transport charges for any future users. The audit explicitly warns that premature construction relative to supply and demand trends leads to unnecessary costs and threatens the viability of the financing mechanism. The logic applies even more strongly once a pipeline is live. Operating an idle asset is not neutral. It actively compounds fiscal exposure.

Affordability concerns reinforce this conclusion. The audit compares projected hydrogen import costs in 2030 of €137 to €318 per MWh with natural gas prices including EU emissions allowances of €43 to €67 per MWh. The resulting gap ranges from €70 to €275 per MWh. Closing that gap through subsidies would require between €3 billion and €25 billion per year for imports alone. Alternatively, carbon prices under the EU emissions trading system would need to rise to between €500 and €1,300 per ton CO2e, compared with prices below €80 in 2025, and far under the EU’s guidance on budgeting for carbon pricing.

The audit does not present cost per ton CO2e abatement figures as the French court of auditors report did, but this omission is telling. The report is clear that climate impacts of hydrogen imports remain uncertain, upstream emissions may dominate lifecycle effects, and hydrogen leakage itself acts as an indirect greenhouse gas, one of the first signals in formal documents that the science on this is being internalized and shaping policy. Under these conditions, precise abatement metrics would give a false sense of accuracy.

The report’s recommendations consistently push toward narrowing hydrogen’s role, even if they avoid explicit sectoral lists. Hydrogen is framed as appropriate only where direct electrification is not feasible, particularly in existing industrial feedstocks and specific high-temperature processes. The audit explicitly states that further uses are not appropriate in terms of energy efficiency and resource conservation. It urges reassessment of sectors previously expected to rely on hydrogen and calls for evaluating alternative decarbonization pathways. This mirrors conclusions reached by the French auditors, even if expressed through budgetary and infrastructure analysis rather than policy prescription.

For the pressurized backbone segment, the implication is uncomfortable but clear. It fails the audit’s own criteria for economic efficiency, synchronization, and risk minimization. Continuing to operate it without credible near-term demand increases the likelihood that the financing mechanism fails and that taxpayers absorb losses measured in tens of billions of euros. The audit explicitly notes that the Federal Network Agency has legal latitude to delay or cancel network sections when demand does not materialize. While it does not issue operational orders, its logic opens the door to de-pressurization, mothballing, or reclassification of such segments as contingency infrastructure rather than active assets.

The deeper governance issue the audit surfaces is the danger of treating sunk costs as strategy. Steel in the ground does not create demand, and pressurization does not make hydrogen inevitable. On the contrary, once infrastructure becomes active without users, it constrains future choices by increasing financial exposure. The audit’s insistence on a plan B is a recognition that persistence alone is not a solution. If hydrogen remains expensive, supply constrained, and demand uncertain through the 2030s, Germany will need alternative pathways to meet climate targets without relying on permanently subsidized hydrogen networks.

In this light, the pressurized hydrogen backbone segment is not evidence of confidence or progress. It is evidence of misalignment between policy ambition and economic reality. The Federal Audit Court’s report makes clear that continuing on autopilot increases risks rather than resolving them. For Parliament and budget legislators, the question is no longer whether hydrogen might play a role in the future, but whether early, idle infrastructure should continue to accumulate costs today in the absence of clear, enforceable energy demand use cases.

Support CleanTechnica via Kickstarter

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy