As the world confronts the dual challenge of decarbonization and energy security, green hydrogen has emerged as a promising solution particularly for economies like India, which must simultaneously meet rising energy demand and reduce carbon emissions. With its ambitious National Green Hydrogen Mission, India has signaled a strategic pivot toward clean fuels that could redefine its industrial base, export potential, and energy independence over the coming decades.

The Case for Green Hydrogen

To understand why India is betting on green hydrogen, let’s begin with the basics.

There are mostly three types of Hydrogen in use:

- Blue Hydrogen

- Grey Hydrogen

- Green Hydrogen

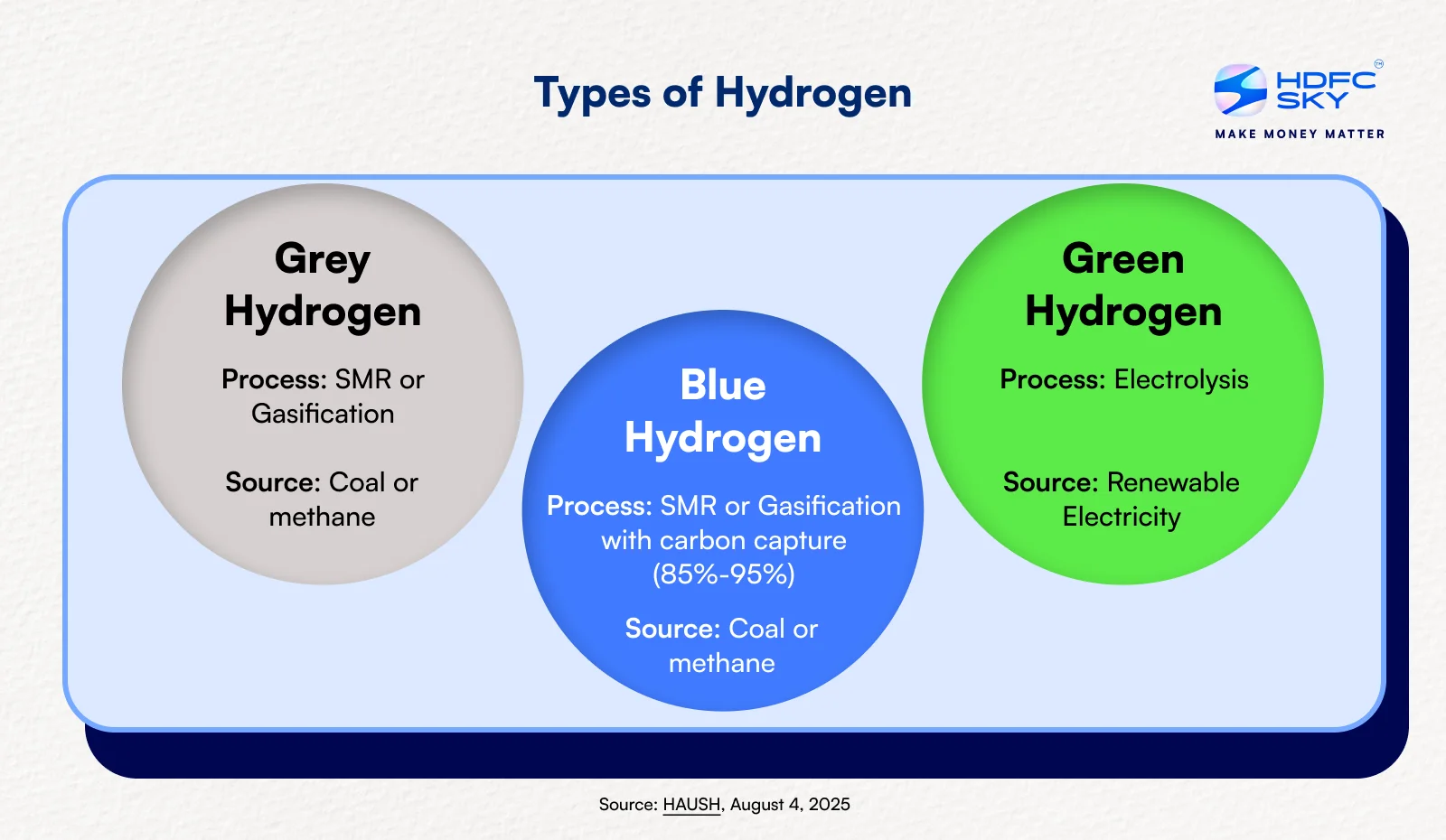

Blue hydrogen is produced from natural gas through a process known as Steam Methane Reforming (SMR), where methane (CH4) is heated with steam to generate hydrogen and carbon dioxide (CO₂). In the case of blue hydrogen, the CO₂ generated is captured and stored using Carbon Capture and Storage (CCS) technology. This involves isolating CO₂ from the reforming process and transporting it to underground geological formations for long-term storage.

That said, the cost of blue hydrogen is largely influenced by the price of natural gas and the high expense and limited efficiency of CCS technologies, especially when scaled for industrial use.

Grey Hydrogen is currently the most widely used form of hydrogen, accounting for approximately 95% of global production. Like blue hydrogen, it is produced through Steam Methane Reforming (SMR) of natural gas. However, unlike blue hydrogen, grey hydrogen does not use Carbon Capture and Storage (CCS), resulting in the direct release of significant amounts of CO₂ into the atmosphere . This makes it environmentally unsustainable in the long run, especially in the context of global climate goals.

Green Hydrogen is produced through a process called electrolysis, where renewable electricity, typically from solar or wind, is used to split water (H₂O) into hydrogen (H₂) and oxygen (O₂). Unlike other forms of hydrogen production, electrolysis generates no direct carbon emissions, making it a clean and sustainable option aligned with global decarbonization goals.

Importantly, the cost of green hydrogen is primarily driven by the price of renewable electricity, which accounts for a significant portion of the overall production expense. As the cost of solar and wind power continues to decline, green hydrogen is expected to become increasingly cost-competitive.

This is particularly relevant for India because it currently imports over 85% of its crude oil and uses hydrogen extensively in sectors like refining and fertilizers, transitioning to green hydrogen is not only a climate imperative but also an economic and geopolitical necessity.

Mission Structure and Strategic Objectives

With this backdrop, the National Green Hydrogen Mission launched in 2023, represents India’s most coordinated push yet into the clean fuel space. The government has committed a total outlay of $2.4 billion , supporting it up to FY 2029-30 .

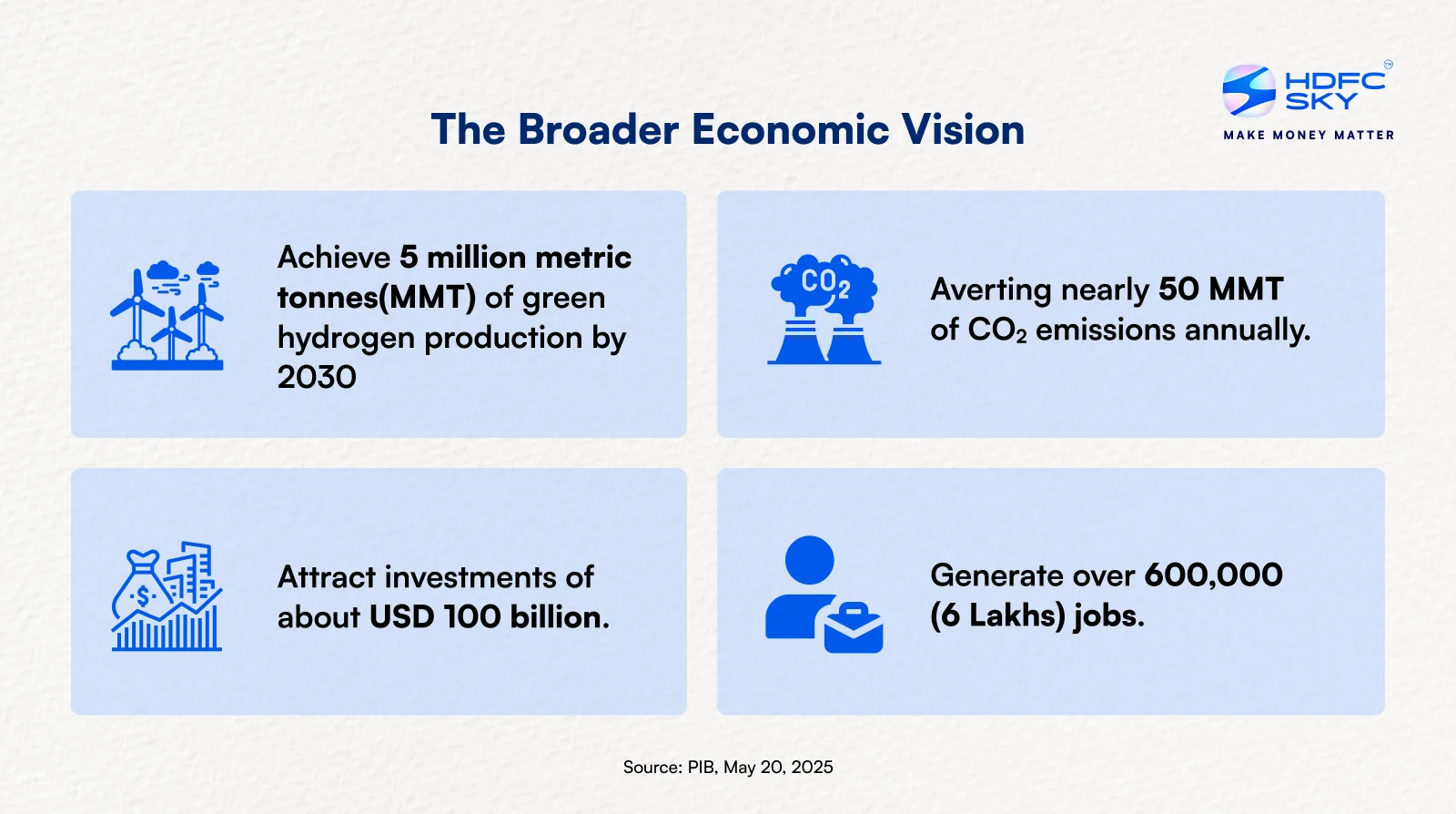

The mission aims to position India as a global hub for the production, utilization, and export of green hydrogen and its derivatives. This aligns with the broader goal of achieving Aatmanirbhar Bharat (self-reliant India) through clean energy and establishing the country as a leading force in the global clean energy transition.

By advancing green hydrogen, the mission will drive deep decarbonization across key sectors, reduce reliance on fossil fuel imports, and enable India to take a leadership role in both green hydrogen technology and global markets.

To realize this ambition of 5 MMT of Green Hydrogen , the country aims to develop around 125 GW of additional renewable energy capacity, with hydrogen plants often co-located with solar and wind farms to minimize transmission losses and costs.

India has set an ambitious vision to attain energy independence by 2047 and achieve net-zero emissions by 2070.

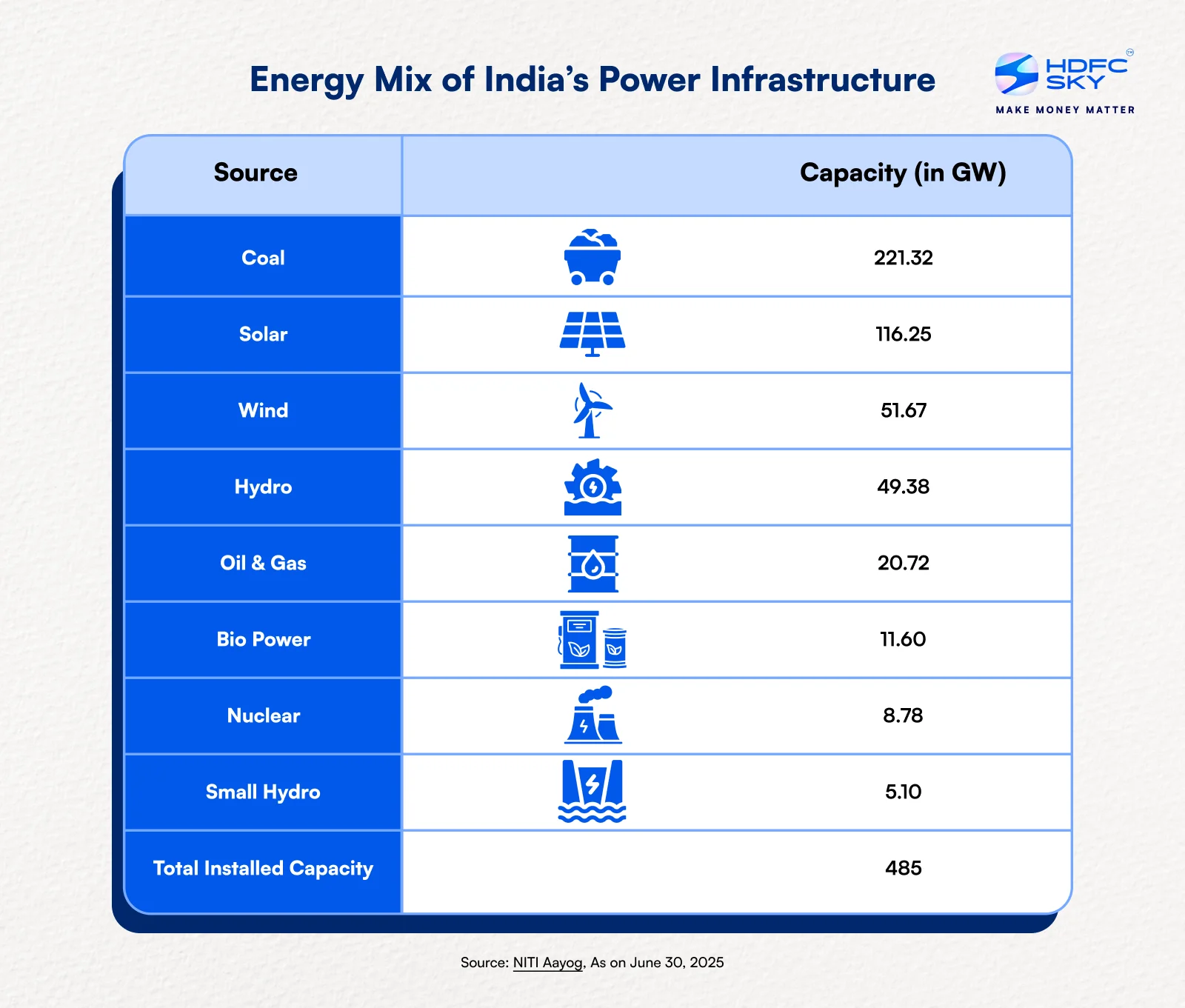

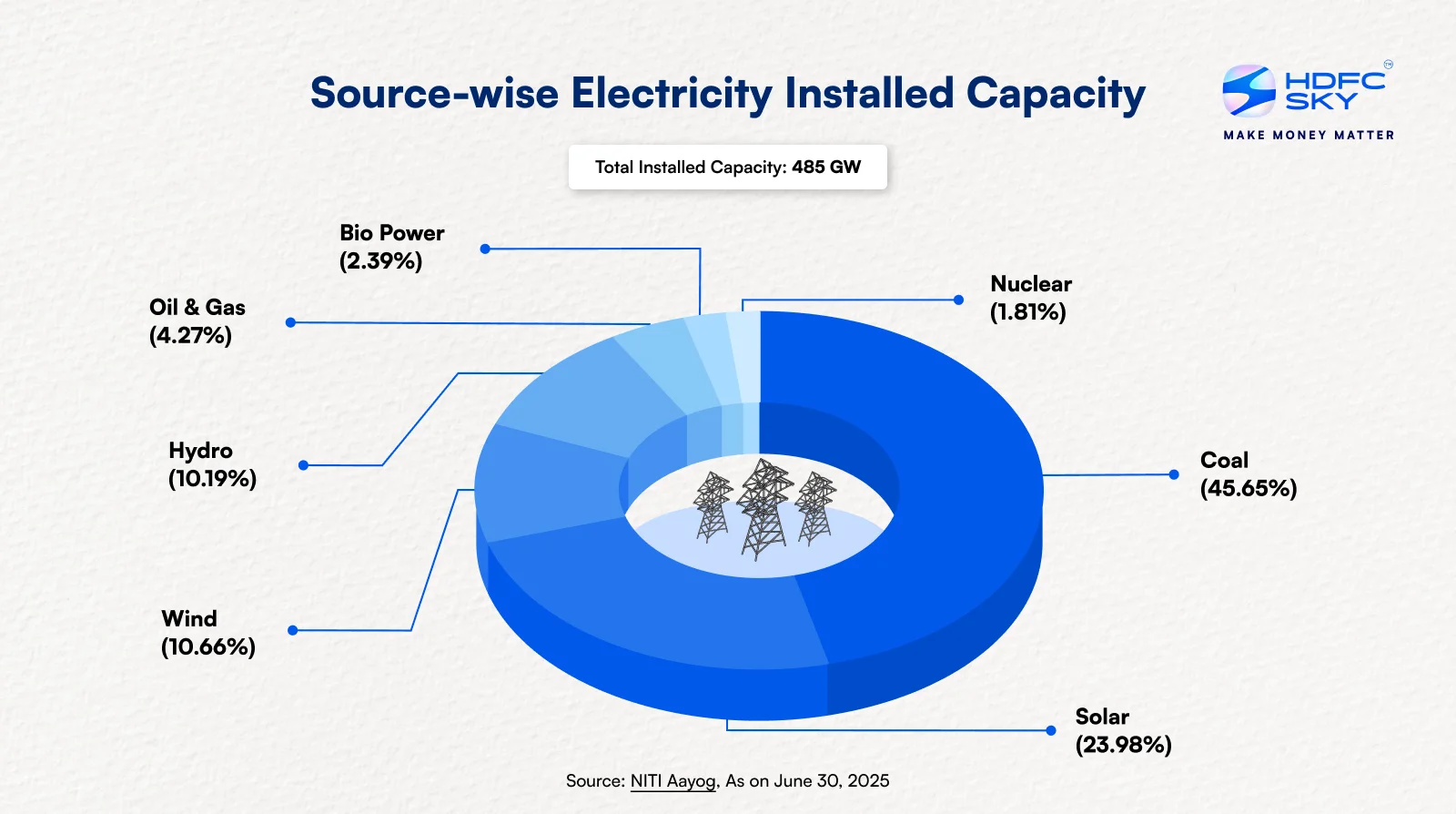

India currently has 116 GW of Solar and 51 GW of Wind in installed capacity as of June 2025.

Policy Mechanisms and Industrial Support

To turn vision into action, the government has put in place several policy levers to catalyze the sector. The Strategic Interventions for Green Hydrogen Transition (SIGHT) programme is a key financial pillar with an outlay of ₹ 17,490 crore up to 2029-30 , offering production-linked incentives to both electrolyser manufacturers and green hydrogen producers.

In addition to direct financial support, the mission includes regulatory reforms such as:

- A 25-year waiver on ISTS charges (Inter-State Transmission Charges) for renewable energy used in hydrogen production, applicable for projects commissioned between March 8, 2019 and December 31, 2030 .

- Provisions such as renewable energy banking and time-bound approval for Open Access and grid connectivity will be extended to support green hydrogen projects.

Projects on the Ground

Despite being in its early stages, India’s green hydrogen ecosystem is rapidly expanding. Several pilot and commercial-scale projects have either been launched or announced over the past two years.

The Deendayal Port Authority at Kandla (Gujarat) recently commissioned India’s first Make-in-India 1 MW green hydrogen plant, with plans to scale it up to 10 MW. This facility is expected to produce over 140 metric tonnes of green hydrogen annually , enough to fuel port operations, buses, and local grid needs.

While traditional sources like coal still account for the largest share of total installed capacity, solar and wind are growing rapidly, and with increased investment in hydrogen production, it is expected to contribute majorly by 2030.

Challenges on the Horizon

While the momentum is strong, several structural and technical challenges remain.

- High Cost of Production and Handling: One of the biggest challenges for India’s green hydrogen ambitions is the high cost of production and handling. To make green hydrogen commercially viable, particularly for hard-to-abate sectors, costs must fall below $2 per kilogram. Achieving this requires bringing down renewable electricity prices to under $0.02 per kilowatt-hour and rapidly reducing the costs of electrolysers. Without these reductions, large-scale adoption will remain out of reach.

- Storage and Transportation Bottlenecks: These are critical challenges in scaling green hydrogen across India. Hydrogen is highly flammable and has a low volumetric energy density, making it difficult and expensive to store and transport safely. India currently lacks dedicated hydrogen pipelines and refueling infrastructure. Without significant investment in a robust, nationwide hydrogen logistics network, even cost-effective production will struggle to translate into end-use adoption.

- Building Robust Demand: In contrast to the enthusiasm on the supply side, demand has remained subdued, and the execution of planned investments has been sluggish. As of 2024, operational green hydrogen capacity, mostly limited to pilot projects, remains below 0.01 million metric tonnes (MMT).

- Water Resource Constraints: This poses a significant challenge for green hydrogen production in India. Producing one kilogram of green hydrogen requires approximately 8.92 litres of demineralised water, a concern in a country already facing water stress. While desalination and wastewater treatment offer solutions, they add to project costs and infrastructure complexity.

- Implementation Gap: While India has outlined plans for over 2 million tonnes per annum (MTPA) of green hydrogen capacity, progress on the ground has been limited. Only a handful of these projects have moved beyond the planning stage to secure final investment decisions or establish firm offtake agreements highlighting a gap between announced targets and actual execution. In fact, under a baseline scenario where just 30% of the projected capacity comes online within the next decade, green hydrogen would still meet only 31% of India’s anticipated demand by 2032, forecasted to reach 8.8 MTPA.

Final Thoughts

Despite the challenges, the fundamentals are promising. India has some of the lowest renewable energy tariffs in the world, a large skilled engineering base, and a government that is increasingly aligned with the green energy agenda. As the cost of electrolyser technology falls and global pressure mounts to reduce carbon footprints, India’s green hydrogen sector could move from policy vision to commercial scale faster than expected.

If executed well, the National Green Hydrogen Mission could do more than just reduce emissions. It could reshape India’s industrial landscape, turn the country into a global green fuel exporter, and ensure a just transition for sectors that are otherwise hard to decarbonize.

In the global race toward net zero, green hydrogen is no longer a distant promise. For India, it may well become a defining pillar of 21st-century energy security and economic growth.

Disclaimer: At HDFC SKY, we take utmost care and due diligence in curating and presenting news and market-related content. However, inadvertent errors or omissions may occasionally occur.

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please note that the information shared is intended solely for informational purposes and does not make any investment recommendations